Table Of Contents

What Are Capital Receipts?

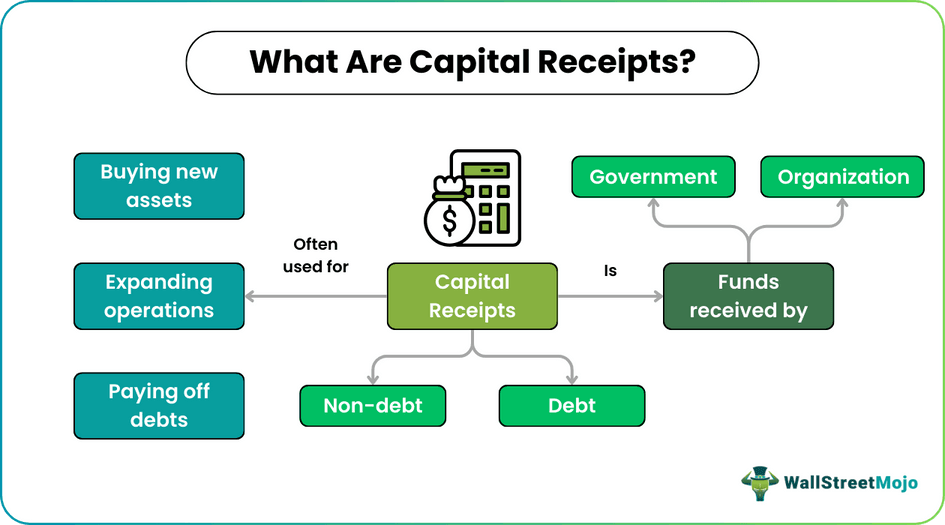

Capital receipts refer to the funds or resources that a government, organization, or individual receives from sources representing increased capital or net worth. These receipts are generally one-time or non-recurring and are not a regular source of income. They aim to raise funds through long-term sources such as equity, debt, and sale of assets to finance capital expenditure.

Capital receipts are recorded in the entity's balance sheet as a liability, representing an increase in the entity's net worth that needs to be accounted for. These funds are important as they are often used for capital expenditure, such as buying new assets, expanding operations, or paying off debts.

Table Of Content

- What Are Capital Receipts?

- Capital receipts refer to the inflow of funds into an entity through the sale of non-current assets, investments, borrowings, and grants used to finance capital expenditures or pay off debt.

- Non-debt capital receipts are funds received by an entity from sources other than borrowing or debt instruments, such as the sale of equity investments, grants, and donations.

- Calculating capital receipts depends on the specific sources of capital inflows an entity has received.

- Capital receipts significantly impact an entity's financial statements as they increase assets or liabilities and cash inflow.

Capital Receipts Explained

Capital receipts are an important aspect of an entity's financial management, representing increased net worth or capital. They are generally non-recurring and are not part of the entity's regular income. Capital receipts are typically used for capital expenditures, such as purchasing new assets or expanding operations.

One of the main sources of capital receipts is the sale of fixed assets. When an entity sells a fixed asset, such as land, buildings, or machinery, it receives a lump sum of cash, which is recorded as a receipt. This money can then be used for other capital expenditures or to pay off debts.

Another source of capital receipts is borrowing. Entities can borrow money through loans or bonds issued, also recorded as a capital receipt. This can be an effective way to raise funds for capital expenditures or other investments.

Grants are also a common source of receipts. Entities can receive grants from government bodies or other organizations, typically earmarked for specific purposes such as infrastructure development or research and development.

Investments and disinvestment can also generate capital receipts. For example, the proceeds are recorded as a receipt when an entity sells investments such as stocks, bonds, or mutual funds. In addition, disinvestment, which refers to the government's sale of equity holdings in a public sector enterprise, can generate receipts.

Capital receipts are an important part of an entity's financial management. They can provide the funds needed for capital expenditures and other investments to help the entity grow and prosper over time.

Types

Capital receipts can be broadly classified into two main types:

#1 - Non-Debt Capital Receipts

These receipts do not create any liability on the entity's balance sheet. They are typically a result of transactions that increase the entity's net worth or capital. Non-debt receipts include the sale of fixed assets, grants received, and investments made by the entity that are later sold.

#2 - Debt Capital Receipts

These receipts create a liability on the entity's balance sheet, as they represent borrowed money that needs to be paid back at some point in the future. Debt receipts include money borrowed by the entity through loans or bonds issued. When an entity borrows money, it receives a lump sum of cash that can be used for capital expenditures or other investments. However, the entity also incurs an obligation to repay the borrowed amount and interest, which is recorded as a liability on its balance sheet.

Both non-debt and debt capital receipts are important for an entity's financial management. They can provide the necessary funds for capital expenditures, investments, and other initiatives to help the entity grow and prosper over time. However, it is important for entities to carefully manage their debt levels and ensure that they have a sustainable plan for paying back any borrowed money.

Components

The components of capital receipts can vary depending on the type of entity and the nature of its operations. However, some of the common components of capital receipts are:

#1 - Sale Of Fixed Assets

This refers to the amount of cash an entity receives for selling its non-current assets, such as land, buildings, machinery, and equipment.

#2 - Borrowings

This refers to the amount of cash an entity receives through loans or bonds. The borrowed amount is recorded as a liability on the entity's balance sheet, and the interest paid on the borrowed amount is recorded as an expense.

#3 - Grants

This refers to the amount of cash an entity receives from government bodies or other organizations for specific purposes, such as research and development, infrastructure development, or social welfare programs.

#4 - Investments

This refers to the amount of cash an entity receives from the sale of its investments, such as stocks, bonds, or mutual funds.

#5 - Disinvestment

This refers to the cash the government receives from selling its equity holdings in a public sector enterprise.

#6 - Miscellaneous Capital Receipts

This refers to any other type not covered by the above categories, such as proceeds from the sale of patents or copyrights.

Overall, the components of capital receipts provide important insights into financial performance and the ability to generate funds for expenditures. Therefore, entities need to manage their capital receipts carefully. In addition, it ensures that they have a sustainable plan for using the funds to grow and prosper over time.

Examples

Let us look at the following examples to understand the concept better.

Example #1

Consider a manufacturing company looking to expand its operations by building a new factory. The company needs to generate funds for this capital expenditure and decides to explore its capital receipt options.

- Sale Of Fixed Assets: The company has non-current assets, such as land and machinery, not used in its current operations. It decides to sell these assets and generates $1 million in capital receipts, which it can use to fund the construction of the new factory.

- Borrowings: The company also borrows $2 million through a bond issue. This amount is a liability on its balance sheet, and the interest paid on the borrowed amount is recorded as an expense. However, the company believes that the returns from the new factory will more than offset the interest costs.

- Grants: The government offers a grant of $500,000 for companies that invest in renewable energy. The company has decided to apply for this grant. It successfully receives the funds, which it can use to offset some of the costs associated with installing renewable energy sources in the new factory.

- Investments: The company has invested in some stocks that have increased in value over time. It decides to sell these stocks and generates $250,000 in capital receipts, which it can use to fund the construction of the new factory.

Overall, the company has generated $3.75 million in capital receipts that it can use to fund the construction of its new factory. This will help the company expand its operations and increase its production capacity, increasing revenues and profits in the long run.

Example #2

Say a local government wants to improve the infrastructure in a particular city area. To do so, it needs to generate funds for this capital expenditure and decides to explore its capital receipt options.

- Sale of fixed assets: The government has non-current assets, such as an old community center that is no longer used. It decides to sell the community center and generates $2 million in capital receipts. This amount can be used to fund infrastructure improvements.

- Borrowings: The government also borrows $3 million through a municipal bond issue. This amount is a liability on its balance sheet, and the interest paid on the borrowed amount is recorded as an expense. However, the government believes that the benefits of the infrastructure improvements will more than offset the interest costs.

- Grants: The government applies for a grant from the state government for infrastructure improvements in the area. It successfully received a grant of $1 million, which it can use to offset some of the costs associated with the infrastructure improvements.

Overall, the government has generated $6 million in receipts that it can use to fund infrastructure improvements. This will help improve residents' quality of life, attract new businesses, and increase property values over time.

Difference Between Capital Receipts And Capital Expenditure

| Features | Capital Receipts | Capital Expenditure |

|---|---|---|

| Definition | Money received by an entity from the sale of non-current assets, investments, borrowings, and grants. | Money spent by an entity on the acquisition or improvement of non-current assets or investments. |

| Nature | Income for the entity. | The expense for the entity. |

| Impact On Financial Statements | Increases assets or liabilities and cash inflow. | Decreases cash and increases non-current assets. |

| Purpose | Used to finance capital expenditure or pay off debt. | Used for long-term investments or to replace, upgrade or add to non-current assets. |

| Timeframe | Usually, they are one-time or infrequent transactions. | Regular and recurring expenses. |

| Examples | Sale of land, equipment or investments, borrowings, grants. | Building or buying a new property, purchasing machinery, upgrading technology or equipment. |

Frequently Asked Questions (FAQs)

Capital receipts are funds an entity receives through the sale of non-current assets, borrowings, and investments. In contrast, revenue receipts refer to income generated by an entity through its regular business operations, such as sales and services.

The repayment of loans is considered a capital receipt because it represents a return of capital initially borrowed by an entity. When an entity borrows money, it receives cash inflows, recorded as capital receipts. Repaying the borrowed money represents a cash outflow that reduces the entity's liabilities and capital base but does not affect its operating income or expenses, which are captured in revenue receipts. Therefore, the repayment of loans is classified as a capital receipt rather than a revenue receipt.

Non-debt capital receipts are funds received by an entity from sources other than borrowing or debt instruments. These receipts are generated through the sale of non-current assets, such as land, buildings, and equipment, as well as through investments, grants, and other equity financing sources. Non-debt capital receipts represent cash inflows that do not create any corresponding liabilities or debt for the entity. They are generally used to finance capital expenditures or add to the entity's equity base.

To calculate capital receipts, determine the specific sources of capital inflows and use the appropriate formula. For example, for the sale of non-current assets, deduct any transaction costs from the sale proceeds to determine the capital receipts. For borrowings, use the total amount of funds received.

Recommended Articles

This article has been a guide to what are Capital Receipts. Here, we explain it with its examples, types, components, and comparison with capital expenditure. You may also find some useful articles here -