Table Of Contents

What Is The CAMELS Rating System?

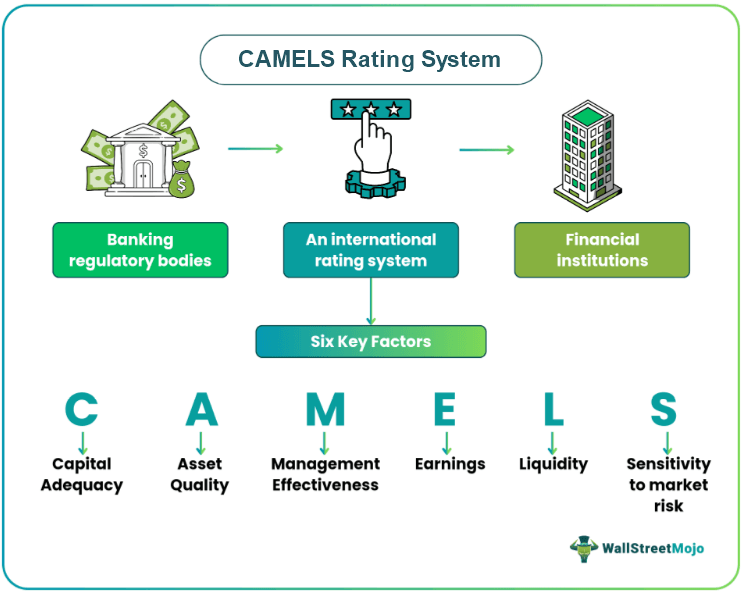

The CAMELS rating system is a globally recognized assessment tool utilized by banking authorities to evaluate banks and financial institutions. The acronym CAMELS represents the six key factors considered when assessing an institution's financial health: Capital adequacy, asset quality, management effectiveness, earnings, liquidity and sensitivity to market risk.

Originally developed in the United States, this rating system is not openly shared; it is exclusively employed by top management to gauge a bank's prospects, current stability, and potential risks. The rating scale ranges from one to five, with one indicating top-tier and strong performance, while five signifies high-risk management practices.

Table of contents

- What Is The CAMELS Rating System?

- The CAMELS rating system is an international rating concept introduced to measure banks and financial institutions.

- It was developed in the US; the FFIEC (Federal Financial Institutions Examination Council) adopted it in 1979, and the NCUA (National Credit Union Administration)adopted the CAMELS rating system in 1987.

- It is based on six factors: capital adequacy, asset quality, management, earnings, liquidity, and sensitivity.

- The rating scale is between one to five, with one showcasing robust performance, whereas five represents high possible risks and managerial issues.

CAMELS Rating System Explained

The CAMELS rating system serves as an international benchmark for evaluating the performance of banks and financial institutions. Although its inception was in the United States, it has been adopted globally. The methodology encompasses six critical financial factors determining a bank's performance, current stability, and future prospects. Originally introduced in 1979 by the Federal Financial Institutions Examination Council (FFIEC) in the United States, it was initially called the Uniform Financial Institution Rating System (UFIRS).

In 1987, the National Credit Union Association (NCUA) began using this system and was responsible for chartering and overseeing federal credit unions. Each of the six factors is individually rated on a scale of 1 to 5, and an average score is calculated to determine the final rating for a bank or financial institution. Those with an average rating of 1 or 2 are deemed high-quality entities, showcasing strong performance and robust financial health. Conversely, institutions receiving ratings between 3 and 5 are considered financially unstable and susceptible to high market risks and potential failure.

The primary purpose of the CAMELS rating system is to identify institutions facing financial challenges, particularly those with insufficient capital reserves. Regulatory bodies then implement stringent measures to facilitate improvements and enforce effective risk management practices. It's important to note that these ratings are not disclosed to the general public. A bank receiving a rating of 4 or 5 can trigger instability in the financial sector and may lead to a bank run.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Components

The CAMELS rating system consists of six key components:

- Capital Adequacy: Capital adequacy involves monitoring and maintaining a minimum capital reserve. The rating is based on both current capital levels and historical records. Capital adequacy depends on the bank's plans and how it allocates its capital, particularly regarding liquidity.

- Assets: The second component assesses the bank's assets and their value. This includes evaluating the value of loans granted by the bank and considering their risk exposure. An institution with significant assets that experience a decline in value may receive a lower rating. Analysts also closely examine other risks, such as interest rate, credit, and liquidity risks.

- Management: The management component evaluates the bank's financial performance, strategies, and ability to respond to financial stress. This assessment encompasses the bank's plans, growth rate, and internal controls for identifying and managing potential risks. It also checks whether the management adheres to established policies, guidelines, and accounting principles.

- Earnings: Bank earnings play a critical role in the CAMELS rating system. Each bank must generate a specific level of earnings to remain competitive and sustain its operations. Various financial ratios, including return on assets and net interest margin, are evaluated to assess the bank's ability to withstand challenging economic conditions.

- Liquidity: Every bank must maintain a minimum amount of liquid capital. In times of financial crisis, a lack of liquid capital can lead to a bank run. Liquidity directly affects an institution's future cash flow and ability to cover daily operational needs. Factors such as interest rates can influence the liquidity ratio.

- Sensitivity: Sensitivity is the final component of the CAMELS rating system, gauging a bank's sensitivity to different market risks. Higher sensitivity is generally not a favorable indicator for any financial institution.

Examples

Here are two examples of CAMELS rating systems; one is hypothetical, and the other is from a real-world scenario:

Example #1

Imagine two banks operating in the same town for over nine years. Using the CAMELS rating system, an analyst evaluates their financial health by thoroughly examining all six components, including liquidity and capital adequacy. After careful assessment, the analyst assigns one bank a rating of 2 and the other a rating of 5.

Although these ratings are not publicly disclosed, banking regulators use them to make important decisions. The first bank with a rating of 2 is allowed to expand by opening more branches and hiring more staff. In contrast, with a rating of 5, the second bank faces increased regulatory scrutiny and restrictions on making changes. This example illustrates how the CAMELS rating system impacts a bank's operations, but the process can be more complex due to external factors.

Example #2

In 2013, JPMorgan Chase, once a stronghold of financial stability, faced a reputation crisis as regulators, investors, and lawmakers scrutinized the bank. The CAMELS rating system was crucial in evaluating the bank's management and financial health. The Office of the Comptroller of the Currency (OCC) downgraded JPMorgan's management rating from "satisfactory" to "needs improvement" after the London Whale trading loss.

The CAMELS rating system assesses key factors like capital adequacy, asset quality, management effectiveness, earnings, liquidity, and sensitivity to market risk. The OCC's assessment indicated that the bank's board and management had failed to properly supervise the Chief Investment Office (CIO) and ensure adequate risk management. This downgrade had regulatory implications, highlighting the importance of maintaining strong management and risk control infrastructure, as evaluated by the CAMELS rating system, in preserving a bank's reputation and financial stability.

Importance

The CAMELS rating system holds significant importance for several reasons:

- Regulatory Oversight: It helps regulators evaluate how well banks and financial institutions are performing and how financially stable they are. This guides regulators in making informed decisions regarding supervision and intervention when needed.

- Growth Opportunities: Banks with good ratings find expanding and engaging in new business activities easier. A higher rating also reassures investors and stakeholders that the bank is well-run and financially healthy.

- Comprehensive Review: CAMELS looks at six vital factors, including a bank's ability to operate and manage risks. This thorough approach ensures a complete assessment of a bank's overall condition.

- Consistent Evaluation: Unlike other methods, CAMELS offers a structured and consistent way to assess a bank's performance. This uniformity makes it simpler to compare and measure banks within the industry.

Advantages And Disadvantages

Advantages of the CAMELS rating system:

- CAMELS ratings provide a straightforward way to assess a bank's performance, making it easier to understand.

- Banks use CAMELS ratings to assess and improve each factor, leading to potential enhancements in their operations.

- CAMELS ratings also cover credit unions, offering a comprehensive assessment of financial institutions and banks.

- The system helps identify weaker banks and problematic institutions, allowing timely intervention.

Disadvantages of the CAMELS rating system:

- The rating system may have some inaccuracy due to inconsistencies in banking records.

- There's a level of subjectivity in understanding and rating banks, as different individuals may interpret the criteria differently.

- CAMELS ratings do not consider many other factors that can directly or indirectly affect a bank's financial health.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

The sensitivity ratio in the CAMELS rating system is important because it assesses a bank's sensitivity to various forms of market risks. This ratio helps regulators and assessors understand how changes in market conditions may impact the bank's financial stability. A higher sensitivity ratio indicates a greater vulnerability to market fluctuations, which can be a red flag for potential risks and the need for improved risk management practices within the bank. It is crucial in evaluating a bank's overall risk profile and financial health.

Yes, CAMELS ratings are confidential. They are not disclosed to the public. These ratings are typically kept confidential among regulators and relevant authorities to maintain the integrity of the assessment process.

Banks that receive a poor rating under the CAMELS system may face increased regulatory scrutiny and intervention. Regulators may require these banks to take corrective measures, improve their financial health, and enhance risk management practices to ensure their stability and protect depositors and the financial system as a whole.

Recommended Articles

This article has been a guide to what is CAMELS Rating System and its full form. Here, we explain it in detail with its importance, components, and examples. You may also find some useful articles here -