Part of our Option Strategies guide

What Is The Call Ratio Backspread?

Call Ratio Backspread is an options trading strategy that involves selling a maximum number of out-of-the-money (OTM) call options while simultaneously buying a lesser number of in-the-money (ITM) call options on the same underlying asset. The primary aim is to profit from a significant upward move in the underlying asset’s price while minimizing the upfront cost or generating a net credit.

The strategy aims to take advantage of a substantial asset price increase, potentially resulting in unlimited profits. The ratio refers to the unequal number of contracts involved in the strategy. This strategy is typically implemented when the trader has a bullish outlook on the underlying asset.

Key Takeaways

- The Call Ratio Backspread strategy is applicable when the trader expects a significant upward price increase.

- The strategy offers profit potential if the underlying asset’s price rises significantly. Profits come from the short OTM calls decreasing in value or expiring worthless, while the long ITM calls increase in value.

- The risk limits the initial cost or debit for the ITM call options. If the underlying asset’s price remains stagnant or decreases, the short OTM calls can retain their value or increase, resulting in potential losses.

Call Ratio Backspread Explained

The Call Ratio Backspread is a trading strategy aimed at profiting from a significant increase in the underlying asset’s price. While it offers the potential for substantial rewards, traders must carefully evaluate the risks involved and tailor the strategy to suit their market outlook and risk tolerance.

If the underlying asset’s price remains stagnant or decreases, the short out-of-the-money calls can retain their value or increase, resulting in potential losses. Therefore, before implementing this strategy, traders must carefully assess market conditions and the underlying asset’s potential for price appreciation.

Its relevance lies in its potential for a high risk-to-reward ratio. The strategy offers the opportunity to profit significantly from a strong upward price movement. This can appeal to traders with a bullish outlook on a particular asset who want to capitalize on its potential growth.

Furthermore, it is applicable in various market conditions. For example, it allows traders to benefit from a bullish market where the underlying asset’s price rises substantially. However, it is also applicable in a volatile market where price swings are present, as the strategy provides exposure to potentially enormous profits if the asset’s price makes a significant move in either direction.

How To Use It?

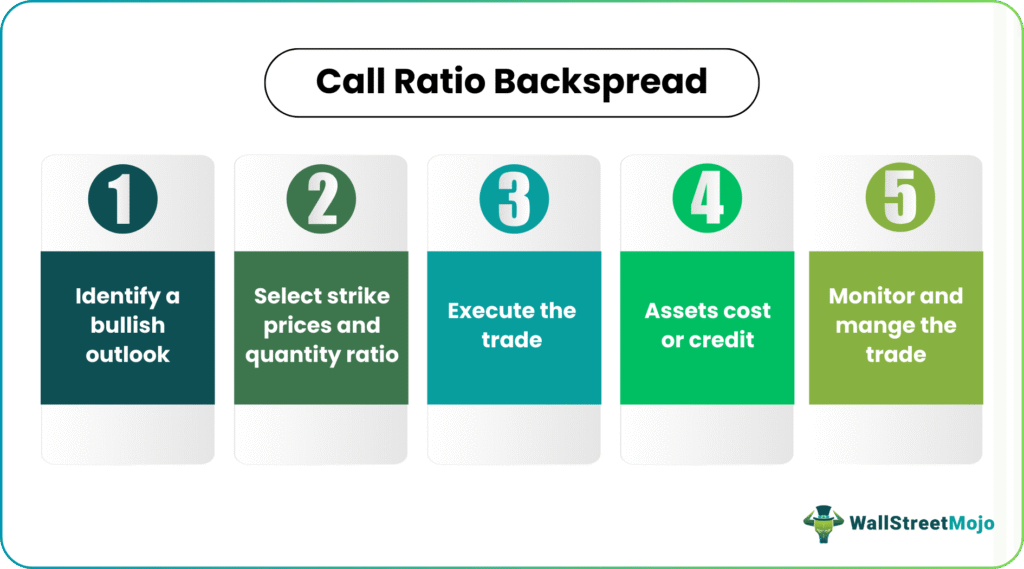

To use the call ratio backspread strategy, follow these steps:

- Identify a Bullish Outlook: Determine that one has a bullish outlook on a particular underlying asset. This means one believes the asset’s price will experience a significant upward move.

- Select Strike Prices: Choose the strike prices for the call options based on analysis and risk tolerance. The OTM call options should have strike prices above the current market price, while the ITM call options should have strike prices below the current market price.

- Determine Quantity Ratio: Decide the ratio of call options one will trade. The strategy involves selling a higher number of OTM call options and buying a lesser number of ITM call options. The specific ratio depends on risk appetite and desired profit potential.

- Execute the Trade: Place the options trades simultaneously. Sell the OTM call options and buy the corresponding quantity of ITM call options. Ensure that the options have the same expiration date.

- Assess Cost or Credit: Evaluate whether the trade results in an upfront cost or credit. Ideally, the strategy aims to generate a net credit, which means one receives more premium from selling the OTM calls than they pay for buying the ITM calls.

- Monitor and Manage the Trade: Keep a close eye on the market and the performance of options positions. If the underlying asset’s price rises significantly, it can lead to profits.

- Potential Outcomes: There are three possible outcomes:

(a) Strong Price Increase: If the price of the underlying asset rises substantially, the short OTM calls may expire worthless or decrease significantly in value, while the long ITM calls increase in value, leading to potential profits.

(b) Moderate Price Increase: If the price rises moderately, the short OTM calls may retain some value, while the long ITM calls may experience limited appreciation. Profits may fall, or the trade may result in a slight loss.

(c) No or Minimal Price Increase: If the price remains stagnant or decreases, the short OTM calls can retain their value or increase, resulting in potential losses.

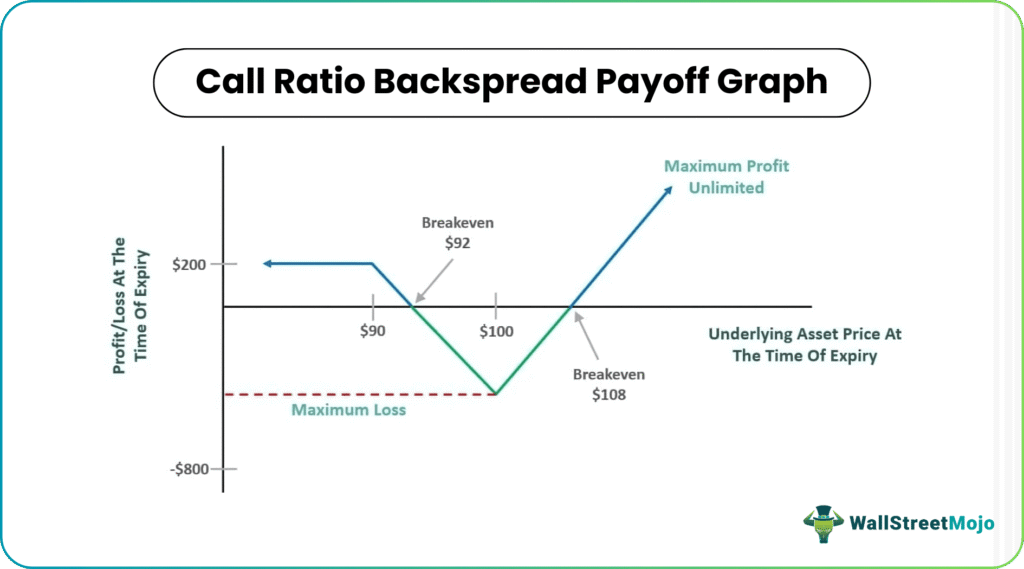

Call Ratio Backspread Payoff

A call ratio backspread graph is V-shaped, where the left side is capped at the overall credit received. While there is unlimited profit potential, the maximum potential loss cannot exceed the spread’s overall width minus the total credit received at the entry.

Traders realize the maximum loss if the closing of the underlying asset takes place at the long call options’ strike price at the time of expiry. During this scenario, the short call finishes in the money or ITM, while the long calls do not have any intrinsic value.

Let us look at the following graph to understand the call ratio backspread payoff concept.

Suppose an asset trades at $96, and per the expectation of Jim, a trader, the security will close over the $100 market at the time of expiry. He entered a call ratio backspread position through 1 sell-top-open or STP $90 call option and 2 buy-to-open or BTO $100 call options.

In case the $90 call option received credit worth $5, and the couple of $100 call options cost $4 each, this position would create credit worth $1 at the entry. If the security is below or at $90 at the time of expiry, every call expires worthless and Jim realizes the initial credit worth $200 as profit.

Note that if the price of the underlying asset is $100 at the time of expiry, the long strike calls would be subject to worthless expiration, and the short call would cost $10 to close. This $10 to close, less the initial credit worth $2, leads to the highest possible loss for the -$800 position.

If the asset is trading over the $100 level at the time of expiry, the loss or profit realized would be equal to the amount obtained by computing the difference between the long call price and asset price, multiplied by the overall long call contracts, less the ITM short call options’ intrinsic value, plus the total credit received initially. For instance, in case the asset closed at 104 at the time of expiry, it would result in a net loss of -$400. Note that the short and a couple of long calls would be ITM $14 and $ ITM $4, respectively. The long calls would gain $800 plus the $100 initial credit, which equals $900. However, the short call would have to close for -$700.

Examples

Let us understand call ratio backspread better with the help of some examples:

Example #1

Suppose Michael is a trader with a bullish outlook on XYZ stock, which is currently trading at $100 per share. Accordingly, he implements a call ratio backspread strategy using options expiring in one month.

He chooses strike prices that reflect his bullish view. For example, let’s say he sells 5 OTM call options with a strike price of $110. And buys 2 ITM call options with a strike price of $95. Michael decides on a ratio of 5:2, where he sells five OTM call options and buys two ITM call options. He simultaneously executes the trades by selling the 5 OTM call options and buying the 2 ITM call options.

After executing the trades, he evaluates the cost or credit. Let’s assume the premium received from selling the OTM calls is $2 per contract. This results in a total credit of $10. The bonus for buying the ITM calls is $5 per contract, resulting in a total debt of $10. In this example, the trade results in a net credit of $10, meaning he receives a $10 upfront credit.

He closely monitors the market and the performance of options positions. For example, if the price of XYZ stock starts rising significantly, his short OTM calls may decrease in value or expire worthless, while his long ITM calls may increase in value, resulting in potential profits.

Potential Outcomes

- If XYZ stock surges to $120 per share, the short OTM calls may expire worthless, and the long ITM calls may significantly appreciate, leading to potential profit.

- If XYZ stock rises to $110 per share, the short OTM calls may retain some value, and the long ITM calls may experience limited appreciation. Profits may be reduced, or the trade may result in a slight loss.

- If XYZ stock remains stagnant or decreases, the short OTM calls can retain their value or increase, resulting in potential losses. However, the risk is limited to the initial debit paid for the ITM call options.

Throughout the trade, Michael applies risk management techniques such as setting a stop-loss order or adjusting the position if market conditions change. Then, he decides when to take profits or close the trade based on his objectives.

Example #2

Recently, the call ratio backspread gained attention in world news related to the options trading activity surrounding GameStop stock (GME) in January 2021.

During that period, a group of retail investors on the Reddit forum r/wallstreetbets initiated a coordinated effort to drive up the price of GME stock. Unfortunately, this caused a significant short squeeze, as institutional investors who had bet against the stock (short sellers) were forced to cover their positions by buying shares, further driving up the price.

Among the various options trading strategies employed by retail investors, some individuals implemented a call ratio back spread on GME options. As a result, they sold many OTM call options while buying fewer ITM call options, similar to the call ratio back spread structure.

These retail investors aimed to profit from the sharp rise in the price of GME stock. Accordingly, they generated upfront premiums by selling OTM call options while limiting potential losses. At the same time, they bought ITM call options to participate in the potential upside.

This strategy attracted attention due to the magnitude of the price movement in GME stock and the subsequent impact on the options market. The coordinated efforts of retail investors using various trading strategies, including the call ratio backspread, resulted in significant volatility and market disruption.

Call Ratio Backspread vs Put Ratio Backspread

The call ratio backspread and the Put Ratio Backspread are options trading strategies investors use to take advantage of anticipated price movements in the underlying asset. However, they differ regarding the market outlook and the types of options involved.

#1 – Market Outlook

The call ratio backspread is employed when the investor has a bullish outlook. It aims to profit from a significant upward move in the asset’s price.

The put ratio backspread is used when the investor has a bearish outlook. It aims to capitalize on a significant downward move in the asset’s price.

#2 – Types of Options

In the call ratio backspread strategy, the investor sells a higher number of OTM call options and buys a lesser number of ITM call options. As a result, the OTM calls have strike prices above the current market price, while the ITM calls have strike prices below the market price.

In the put ratio backspread strategy, the investor sells a higher number of OTM put options and buys a lesser number of ITM put options. As a result, the OTM puts strike prices below the current market price, while the ITM puts strike prices above the market price.

#3 – Profit Potential

The call ratio backspread offers profit potential if the underlying asset’s price rises significantly. For example, the short OTM calls may expire worthless, while the long ITM calls increase in value.

The put ratio backspread also offers profit potential if the underlying asset’s price decreases significantly. For example, the short OTM puts may expire worthless, while the long ITM puts increase in value.

#4 – Risk

The risk in a call ratio back spread is limited to the initial cost or debit paid for the ITM call options. If the underlying asset’s price remains stagnant or decreases, the short OTM calls can retain their value or increase, resulting in potential losses.

The risk in a put ratio backspread is also limited to the initial cost or debit paid for the ITM put options. If the underlying asset’s price remains stagnant or increases, the short OTM puts can retain their value or growth, leading to potential losses.

Frequently Asked Questions (FAQs)

1.How do I calculate the breakeven point for a Call Ratio Backspread?

The breakeven point is where the profits from the ITM call options offset the losses from the short OTM call options. It can be calculated by adding the strike price of the ITM call options to the net premium received or subtracting the net premium paid. However, it’s advisable to use options analysis software or consult with a financial professional for accurate calculations.

2.What is the ideal ratio for a Call Ratio Backspread?

The ideal ratio can vary depending on the trader’s risk appetite and market conditions. Common ratios include 2:1 or 3:1, where the trader sells two or three OTM options for every ITM option purchased. However, the balance can be adjusted based on the trader’s outlook and desired profit potential.

3.Can a Call Ratio Backspread be adjusted or managed after implementation?

Yes, it can be adjusted or managed after implementation. For example, traders can close or change their position based on market conditions, price movements, or risk management approaches. Adjustments can involve rolling the options, adding or reducing contracts, or implementing stop-loss orders to manage risk.

Recommended Articles

This has been a guide to what is Call Ratio Backspread. Here, we explain its examples, how to use it, and compare it with put ratio backspread. You can learn more about it from the following articles –