Table Of Contents

Call Loan Meaning

A call loan (CL) is a type of short-term loan that the borrower must repay immediately at the lender's request. Typically, financial institutions extend such loans to brokers or brokerage houses to meet their short-term capital needs. This type of loan reduces the financial risks associated with lending.

Banks charge interest on CLs and use securities as collateral to secure them. Thus, CLs enable banks to earn income on their idle funds, maintain liquidity, and minimize their credit risk. At the same time, CLs offer instant funds to the brokerage firms to finance the margin account of their clients. Therefore, it is also called broker loans, call money, or overnight broker loans.

Table of contents

- Call Loan Meaning

- A call loan is a short-duration loan that is repayable at the lender’s request or the borrower’s discretion. It is usually for a duration of 1-14 days.

- Banks provide call loans to brokerage houses to finance their stock purchases in return for interest.

- The call loan rate (CLR) is the rate of interest that banks charge on call loans.

- Call loans are a bit risky for the borrowers as the lenders may demand repayment at any time.

- They are highly liquid assets as they may be converted into cash on short notice.

Call Loan Explained

A call loan is a short-term credit that must be repaid to the lender on demand. It comes with a maturity of one to 14 days. If the duration of such a loan is one day or overnight, it is called an overnight loan. However, if it extends to 14 days, it is called notice money.

The payment of a CL is based on the borrower's or the lender's discretion. For example, X lends some money to Y for 14 days. However, X needs money before the maturity of the loan. In this case, X can call upon Y to repay the amount. Similarly, if Y doesn't need the funds, he can return the money to X as and when required.

CLs have high liquidity as the lender or borrower can receive or make the payment at any time before maturity. It fulfills the funding needs of the borrower and benefits the lender in the form of interest on the loan. The rate at which lenders provide the loan is called the call loan rate (CLR). It fluctuates on a daily basis.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

How Does A Call Loan Work?

The call-loan market of New York flourished during the early part of the 1900s. There were several trust companies in New York during this time. They played a major role in the call loan market. These trusts gave huge sums as loans to stock market brokers directly without any collateral as they required these loans to be paid at the end of every business day.

Brokers used these CLs to buy securities either for themselves or to finance the margin accounts of their clients. Moreover, these securities were then kept as collateral for the CL to expedite stock purchases from various national chartered banks. Furthermore, the brokers collected the profit from the stock trading and repaid the loan of the trusts at the end of every closing of the stock markets.

Currently, the trusts have given way to banks and other financial institutions. These banks offer the brokerage houses the much-needed CLs. The brokerages, in turn, give them to their clients as margin loans for buying stocks. In exchange, the banks receive interest at CLR. Usually, banks don’t call the loans daily, so they get rolled over.

As and when the banks demand repayment, the brokers settle them by selling securities or taking other CLs. As evident, CLs increase the stock exchange liquidity. However, it comes with its share of risks.

If several banks call in their CLs at the same time and are unwilling to lend, then brokers may be forced to sell off their holdings at lower prices to make good the payment. This may result in potential losses to investors and even pull down the stock prices leading to a stock market crash.

Examples

Let us look at the following examples to understand the concept better.

Example #1

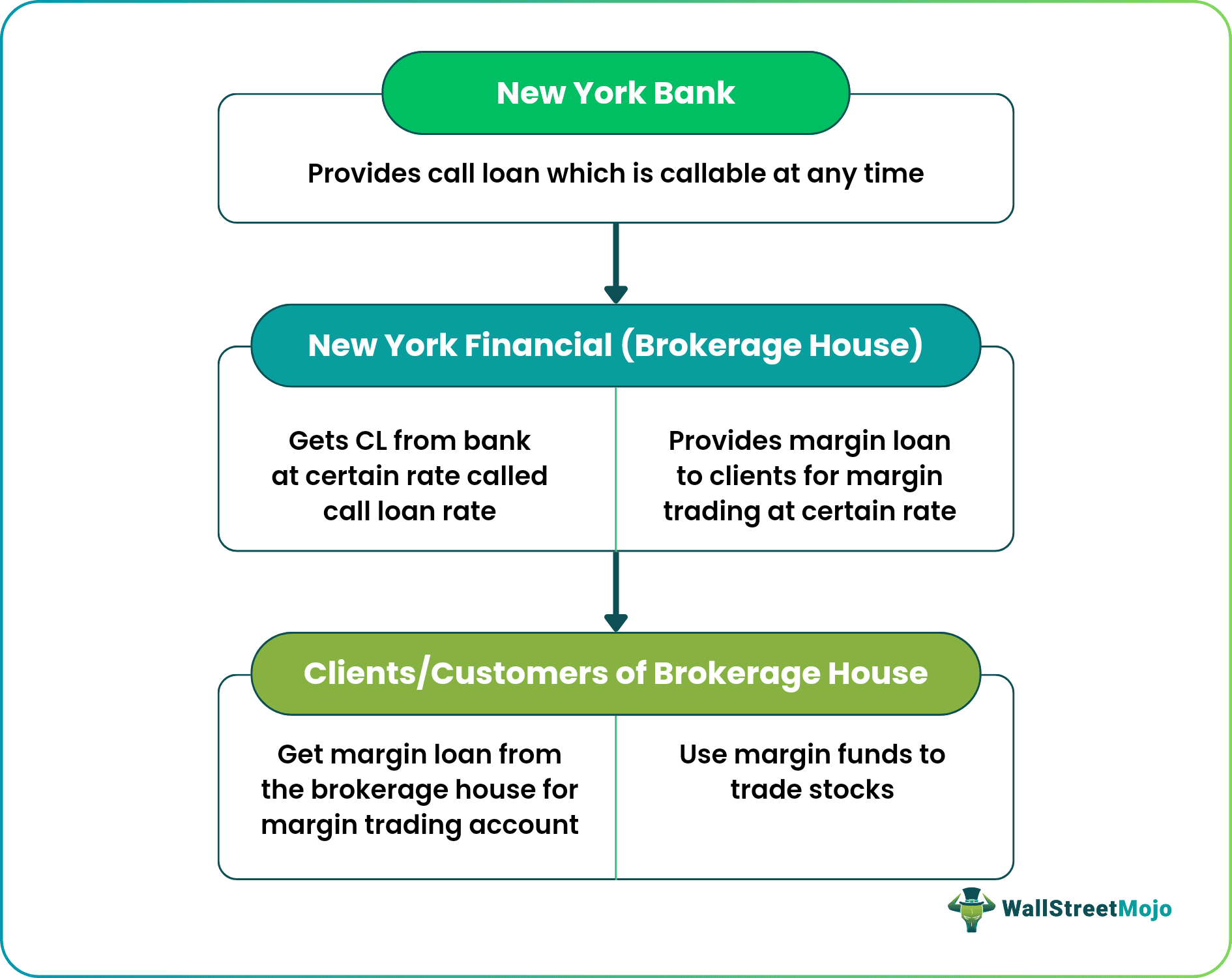

Let us suppose a brokerage house named New York Financials (NYF) approaches a New York Bank (NYB) for short-term funds to utilize in its stock market business. The NYB gives a loan to NYF for 14 days at a certain rate. Since the loan is for a short duration and is repayable on demand, it will be a CL for NYF. This loan will be backed by securities which NYF will offer NYB.

In this case, NYF will have to pay interest to the bank at a CLR rate. At the same time, it may use this CL to offer margin loans to its clients or investors. In order to gain more on stock trading, the investors borrow money (margin loan) from brokerages to invest in high-performance stocks by keeping their stock as collateral.

When the business hours of the stock end, the margin loan gets rolled on for another day, and the brokerage house gets a certain fee at a margin rate (CLR plus premium). NYF will pay interest (CLR) to the bank for the loan from this fee.

Now, suppose the prices of the securities kept as collateral with NYB fall, and the bank feels the need to call back its loan after a week. Then, it can intimate NYF. NYF must sell securities or take another CL to settle the NYB CL immediately.

Example #2

Now let's take an example of a bank-to-bank transaction involving a call loan. Unfortunately, many smaller banks do not have enough funds or liquidity to lend to bigger account holders or pay their customers.

These banks also utilize the concept of CL and borrow funds from bigger commercial banks at CLR for a short duration that has to be paid back at the lender's discretion. This measure solves their short-term needs of liquidity and other funding needs.

Sometimes, commercial banks also take CLs to maintain their cash reserve ratios with the country’s central bank.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

This loan is important to maintain healthy liquidity in stock markets and meet the funding needs of several small banks and brokerage houses.

The call loan rate (CLR) is the rate of interest that banks charge on call loans. Brokerage houses pay them to receive funds to fund their temporary capital needs. Call rates are subject to fluctuations and are determined on a daily basis. They are published in several leading periodicals.

This loan has pros for lenders as they can ask for the repayment of the loan at any time and earn a fixed rate of interest as well. The loans are also backed by securities, so lenders have protection against default. Though borrowers get funding for their capital requirements, borrowers have to pay interest on the loan and face the risk of selling stocks at low prices to pay back the lender on short notice.

Since the securities backing the call loans are highly volatile, any reduction in their value may trigger calls for repayments by banks. Moreover, in the event of a banking crisis, it may be difficult for brokers to obtain CL from other banks. So, they will have to sell off their securities at lower prices to pay back the banks. This may cause the stock prices to drop further, resulting in a stock market crash. The great financial crisis of 1907 in New York stands witness to it.

Recommended Articles

This article has been a guide to Call Loan & its Meaning. Here we discuss the concept of call loan and its rates along with their explanation and examples. You can learn more from the following articles –