Table Of Contents

What Is A Buydown?

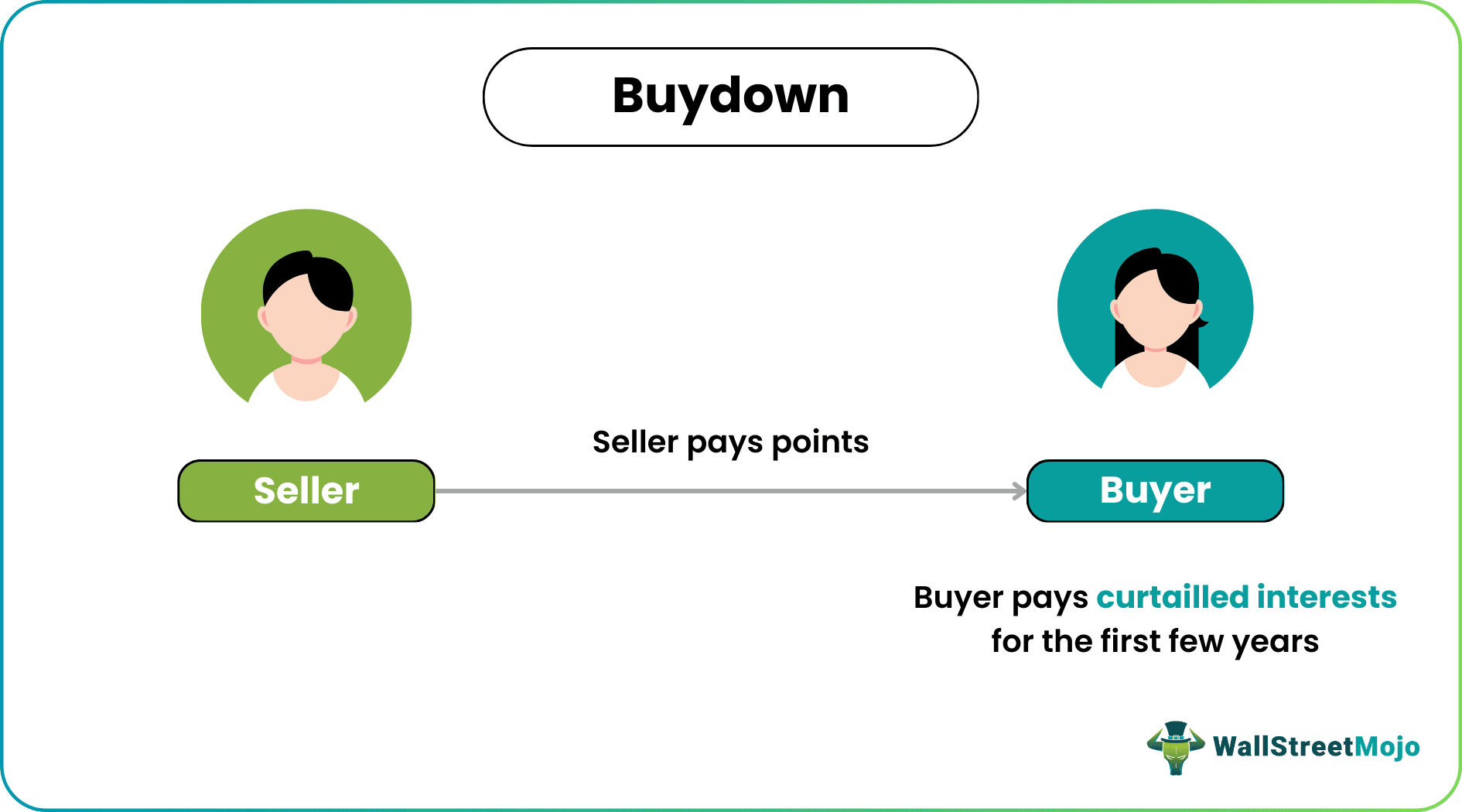

A buydown or a temporary buydown is a provision where the borrower or a third party pays a lumpsum fee. In lieu, the borrower pays a curtailed interest every month. Typically, the reduction in interest lasts for a short duration, one to three years. A buydown aims to provide the borrower with lower monthly mortgage payments for a set period, allowing them to qualify for a larger loan or make the payments more affordable.

This structure helps borrowers transition from lower to higher monthly payments in a gradual manner. It is especially convenient for borrowers who foresee an increase in wages within a few years. Realtors and developers promote these discounts, hoping they can close more deals.

Table of contents

- What is a Buydown?

- A buydown in a mortgage is a financing technique. Sometimes, lenders offer a cheaper interest rate during the initial years of the loan.

- In the 3-2-1 structure, mortgage interest is curtailed by three percentage points during the first year. In the subsequent years, interest is reduced by 2 points and 1 point, respectively.

- A 2-1 buydown structure resembles a 3-2-1 structure. Instead of three years, the 2-1 curtails interests only for the first two years.

- Curtailed interests promote increased purchases, but they come with associated risks. The lenders are exposed to increased default risks.

Buydown Agreement Explained

A buydown is a mortgage financing technique where the lender can offer the buyer a cheaper interest rate during the initial years of the loan. In exchange for the low-interest mortgage, the borrower pays a fee—this can be arranged in various ways.

A temporary low-interest mortgage lasts for a shorter period than the loan's entire duration. Usually, temporary low-interest mortgages do not allow cash-out refinancing, expedited (streamlined) refinancing, or loans secured by a property.

Typically, lenders employ two structures—the 3-2-1 low-interest mortgage and the 2-1 low-interest mortgage structure. Of course, this is in addition to buydowns during the loan. But, irrespective of the framework, the same fundamentals apply.

In low-interest mortgages, the difference between the standard interest rate and the decreased rate will be paid to the lender at the end of the low-interest provision. The borrower benefits from low interest when the low-interest mortgage is active—usually in the first few years. Again, it is important to note that once the provision expires, the borrower pays the full interest.

According to Fannie Mae, buydown agreements should include the following:

- The borrower is not relieved of their obligation to make mortgage payments as per the terms if, for any reason, buydown funds are unavailable.

- There is a provision for funds to be returned to the borrower or lender if the mortgage is paid off before buydown funds have been applied.

Borrowers must include a copy of the low-interest mortgage agreement in the mortgage delivery documentation.

These arrangements are especially helpful when a homeowner (mortgage borrower) relocates—within a short span, they can either trade up to a better house or downsize. Moreover, new houses require new furniture and renovation; a curtailed interest comes in handy.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

3-2-1 Buydown

To lower the mortgage rates on houses, sellers make up-front payments. However, developers prefer low-interest mortgages; they let builders offer discounts without lowering their list prices.

With a 3-2-1 buydown, a buyer pays a curtailed mortgage interest for the first three years. The interest rate is reduced by 1% (or more) for the first three years—depending on the amount paid upfront. For example, a 3-2-1 buyer receives a 3% reduction in mortgage interest during the first year, a 2% reduction in the second year, and a 1% reduction in the third year. From the fourth year onwards, the buyer is responsible for making the entire payment.

2-1 Buydown

A 2-1 buydown resembles the 3-2-1 structure; instead of three years, the mortgage is curtailed for two years (first two years). In addition, interest is curtailed by 2% for the first year and 1% for the second year. Real estate agents offer these provisions to complete more deals. So these provisions benefit both parties.

Example

Now, let us look at a buydown example to understand mortgage better.

Dan opts for a low-interest mortgage and borrows $1000,000. A 5% interest is imposed on the loan, and the loan tenure spans 25 years. Dan opts for the 3-2-1 structure.

If the low-interest mortgage fee is $50000, Dan pays the following amount:

1st Year: Interest Rate is Curtailed by 3%

- If he does not buy points, the payment amount is $5,846.

- If he buys points, the payment amount is $4,239.

- There is a difference of $1,607.

2nd Year: Interest Rate is Curtailed by 2%

- If he does not buy points, the payment amount is $5,846

- If he buys points, the payment amount is $4,742

- There is an interest reduction of $1,104.

3rd Year: Interest Rate is Curtailed by 1%

- If he does not buy points, the payment amount is $5,846

- If he buys points, the payment amount is $5,278

- The interest is reduced by $568.

4th Year: Full interest of 5%

- The payment amount is $5,846.

Dan saves a lot in the initial years of loan repayment.

Risks

Now, let us look at buydown risks.

The individual must have sufficient liquidity to afford a significant down payment. Also, when the reduction in interest is lifted, there is a significant increase in monthly payments. Sometimes, borrowers cannot meet the sudden increase in monthly expenses—buydowns are subject to increased default risks.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Here, the borrower makes a lump sum payment to lower the loan interest rate for a short span—initial years.

In a low-interest mortgage, interest is curtailed by a percentage; this percentage is referred to as discount points, mortgage points, or prepaid interest points. For example, by paying an upfront fee, a borrower avails a discount of three percentage points for the first year, 2 points for the second year, and 1 point for the third year.

It depends on the individual buyer; if they can afford the down payment, then it can come in handy. This reduction in monthly expenses can instead be spent on remodeling, renovation, furniture, expansion, etc.

Recommended Articles

This has been a guide to what is Buydown. Here, we explain it in detail with the 2-1 and the 3-2-1 structure, its risks, and an example. You can learn more about it from the following articles –