Table Of Contents

What Are Banking Fundamentals?

Banking fundamentals are the principles and concepts related to banking, an industry dealing with storage for cash and credit facilities, in addition to financial transactions. Individuals must understand the fundamentals to learn how banks serve as a link between borrowers and depositors.

Banks carry out various functions, such as forex trading, currency exchange, deposits, wealth management, and withdrawals. There are different types of banks, like commercial or corporate, investment, and retail. In the United States, individual states and the Federal Reserve regulate banks. In most countries, the banking industry is a vital driver of the economy.

Kay Takeaways

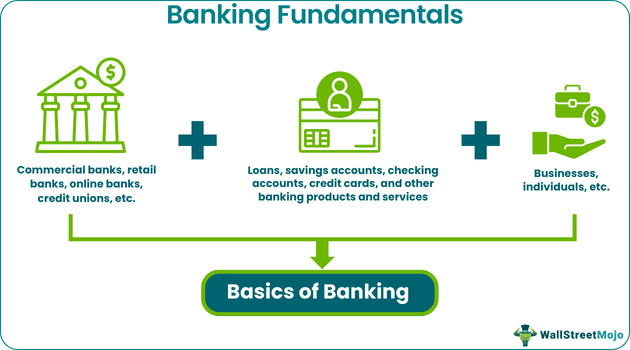

- Banking fundamentals refer to the nuts and bolts of the banking practice. The key elements of commercial or retail banking are the different types of banks, the various banking products and services, and the end customers.

- Some of the different types of banks are commercial or corporate, retail, central, and online banks.

- The different products and services offered by banks include home loans, business loans, credit and debit cards, a safe deposit box facility, etc.

- A certificate of deposit, checking account, and savings account are the three types of bank accounts available at a bank.

How Do Banks Work?

Banking fundamentals refer to the basics concerning the concept of banking. Banks utilize customers’ deposits to offer credit facilities to individuals or entities. As a result, they establish a connection between borrowers and depositors. These financial institutions generate income by charging a rate of interest on the financial assistance or loans provided. Note that the interest rate at which they provide loans is higher than the rate offered on customer deposits.

Based on the business structure, banks in the United States may have to adhere to state regulations, national regulations, or both. Every state’s Department of Financial Institutions or Department of Banking regulates state banks. Generally, such an agency is responsible for addressing issues like what rate of interest a bank can charge, permitted practices, and inspecting and auditing banks.

As part of core banking fundamentals, banks must retain a minimum of 10% of every deposit made on hand to fulfill the Federal Reserve’s reserve requirements. They can provide the remaining 90% as loans. The Board of Governors of the Federal Reserve determines the reserve requirement. This requirement is applicable to all banks that have the license to conduct operations in the U.S.

When the Federal Reserve increases its reserve requirement, it tries to reduce liquidity. On the other hand, when the Federal Reserve lowers the reserve requirement, it tries to increase the flow of money within the economy.

Individuals must note that besides meeting the reserve requirement, all member banks must be insured by the Federal Deposit Insurance Corporation (FDIC). This government organization provides coverage of up to $250,000 for each account per institution, per depositor, to safeguard individuals in the event of a crisis.

Tarjetas Online ES is an informational website that provides comparisons and insights on various banking and card products available in Spain. It offers helpful overviews of debit, credit, and prepaid cards, making it easier for users to understand the options available and choose products that fit their financial needs.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Banking Services

Typically banks worldwide offer an extensive range of services to cater to the requirements of their customers. It is vital to know them to understand commercial bank principles. So, let us find out what they are.

#1 - Business Banking

This refers to the financial services offered to business owners needing to differentiate between personal and professional finances. In this segment, the different services provided by banks are as follows:

- Checking accounts

- Business loans

- Savings accounts

- Credit and debit cards

Additionally, banks offer treasury services (deposit services, payroll services, etc.) and merchant services (check collection, reconciliation and reporting, credit card processing, etc.)

#2 - Individual Banking

This includes the services banks provide to aid individuals in fulfilling their financial requirements. Such services include credit and debit cards, savings accounts, checking accounts, wealth management, a safe deposit box facility, home loans, and insurance.

#3 - Digital Banking

Digital banking enables individuals to manage their finances from their preferred location via a computer, smartphone, or tablet. This facility is becoming increasingly crucial for consumers. Typically, the digital services banks offer are eStatements, text alerts, online banking, online bill payment facility, and mobile check deposit.

Types Of Banks

Let us look at the different types of banks to understand core banking fundamentals better.

- Retail Banks: Understanding the meaning and functions of retail banks is crucial to knowing retail banking fundamentals. Typically, individuals are familiar with this type of bank as they usually keep their savings and checking accounts with it. These banks’ primary customers are the general public or consumers.

- Commercial Banks: Such banks’ main customers are businesses. Hence, they are also known as corporate banks. Manage payments, offer business loans, offer lines of credit, and provide services related to foreign exchange to businesses carrying out operations overseas.

- Investment Banks: These banks help organizations raise funds in financial markets. Moreover, such banks offer services when companies want to float their initial public offering (IPO). Moreover, they offer advice regarding mergers and acquisitions.

- Central Banks: This type of bank manages a government’s monetary system. For instance, the Federal Reserve is the central bank in the United States. It supervises banks and sets the monetary policy to keep inflation in check.

- Online Banks: These banks conduct operations entirely online. This means they have no physical branch. Usually, these banks offer competitive interest rates on a savings account.

- Savings And Loan Institutions: Although such banks are less prevalent, they remain important. This type of bank played a crucial role in making homeownership mainstream. It used customers’ savings deposits to offer home loans.

- Credit Unions: They are like banks. However, they are customer-owned and non-profit. Their offerings are more or less the same as retail banks.

- Mutual Banks: These banks are like credit unions since customers or members own them.

Types Of Bank Accounts

One must know the different types of bank accounts is vital to understand banking fundamentals. So, let us find out what they are.

#1 - Checking Out

Such an account enables customers to access the funds they deposited easily. Moreover, one can use such an account to carry out financial transactions, for example, making bill payments. Note that customers can write a check to access funds. Moreover, they may use their debit card to make payments or withdraw money. Besides these, they can set up automatic transfers.

#2 - Savings Account

This refers to a bank account where customers can deposit funds they do not require immediately. The money is available for instant withdrawal if the person requires it. Banks loan out the deposited funds to borrowers and charge interest on the loan amount.

#3 - Certificate Of Deposit

This is a bank account in which individuals keep a fixed sum for a certain period, like a year, two years, or six months. Such an account offers a fixed rate of interest on the money held.

Examples

Let us look at a few banking fundamentals examples to understand the concept better:

Example #1

Suppose Sam visited his nearest bank branch to deposit $2,000 in his checking account. After depositing the amount, he enquired about a home loan. After knowing the interest rates, tenure options, etc., Sam went home and applied for a mortgage using the bank’s Internet banking facility. Within a few minutes, he completed the application procedure. The bank disbursed the loan amount within a few days after verifying the required documents submitted by Sam.

Example #2

In July 2023, Wells Fargo was facing a technical problem. As a result of the issue, its customers reported that the direct deposits they made disappeared from their accounts. On Twitter (now ‘X’), an individual said that an overdraft fee was charged after his funds disappeared from his account.

On August 4, a spokesperson from Wells Fargo said to CNN that a certain number of their customers were not able to see the recent deposit transactions performed by them. The person also apologized for the inconvenience caused and said that most of the issues were resolved, and only a few remained. The customers of Wells Fargo also faced a technical glitch in March 2023.

Importance

Individuals must be aware of the importance of banking to comprehend banking fundamentals fully. So, let us look at some importance that highlights the importance of this practice.

- Banks enable individuals and organizations to store their funds securely.

- Federal laws safeguard depositors’ money from fraud.

- Individuals can access their money faster than they could using a paper check.

- One can acquire multiple financial products, like credit cards, loans, etc., from banks to easily meet their financial requirements.

- Digital banking allows one to make payments from the comfort of their home.

- Individuals can have proof of payment if they make payments through a bank account.

- Banking allows people to monitor their savings.

- One can withdraw cash easily because of banks’ vast ATM network.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Safety, purpose, liquidity, and profitability are key principles the different types of banks, such as commercial or corporate and retail, must follow to eliminate losses and fraud.

Some key issues related to banking are as follows:

- Security breaches

- Changing business models

- Increasing expectations

- Regulatory compliance

- Customer retention

- Outdated mobile experiences

- A cultural shift

Credit risk is the most significant risk associated with banking. This risk arises when counterparties or borrowers are unable to fulfill contractual obligations. For instance, credit risk occurs when a borrower defaults on the interest or principal payment. Note that defaults may occur on fixed-income assets, credit cards, and mortgages.

There are multiple noteworthy disadvantages. Some of them are as follows:

- Absence of actual bank branches

- No assistance offered by a personal banker

- Tech-associated service disruptions

- Deposit-related restrictions, etc.

Recommended Articles

This article has been a guide to what are Banking Fundamentals. Here, we explain its examples, banking services, bank and bank account types, and importance. You may also find some useful articles here -