Table Of Contents

What Is A Bank Stress Test?

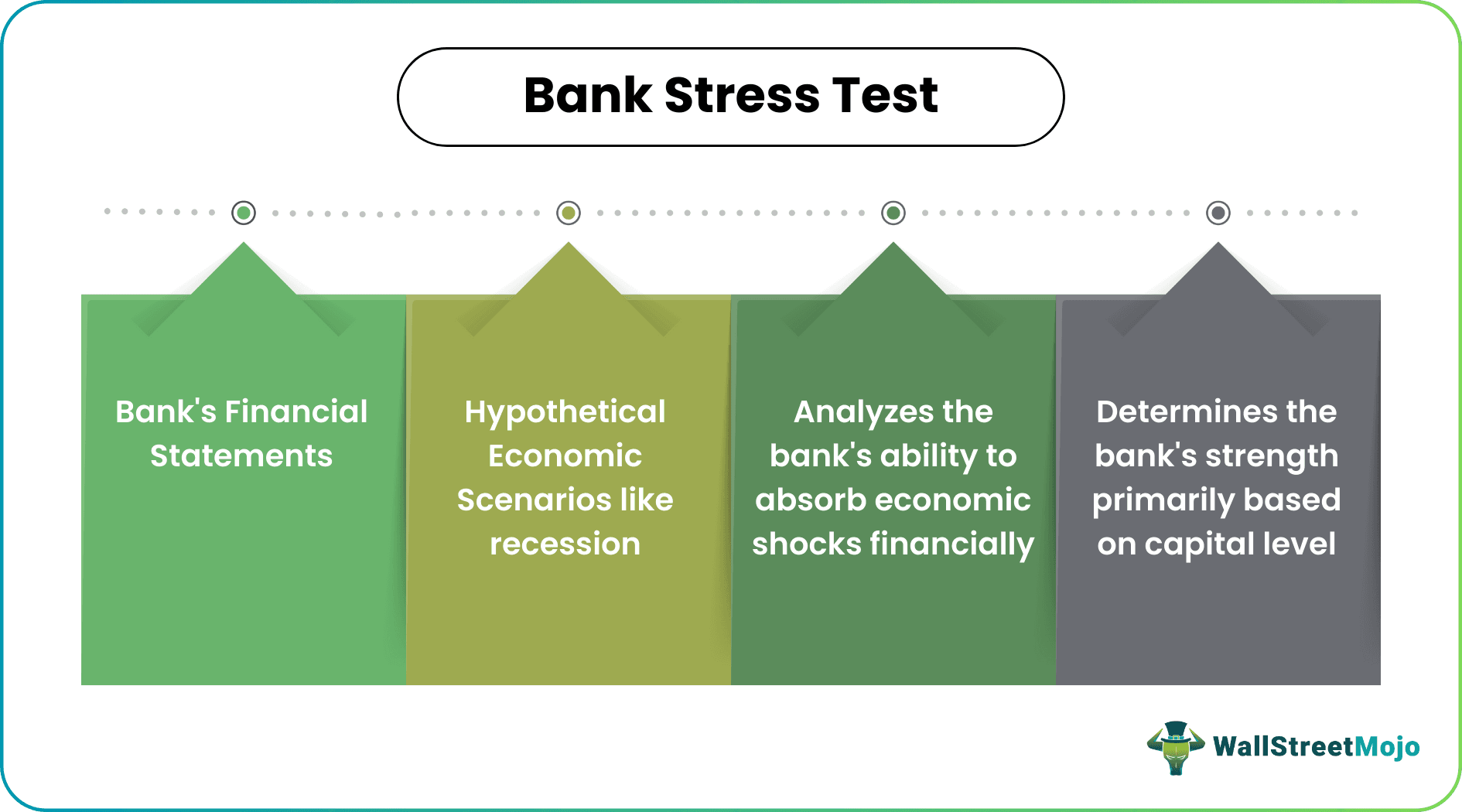

A bank stress test is an assessment performed to determine a bank's financial health and ability to endure economic adversity. The stress test aims to offer investors with meaningful information, increase bank operations transparency, and boost consumer trust.

It is a reliable method for analysing the quality of the banking sector. The test result will help the organizations to protect themselves from failures by taking precautionary measures.

Table of contents

- What is a Bank Stress Test?

- Bank stress test is an examination conducted primarily to scrutinize bank's financial viability when exposed to difficult operational conditions in domestic and international markets.

- In the United States, stress test conducted by Federal Reserve includes Dodd-Frank Act Stress Test (DFAST) and Comprehensive Capital Analysis & review (CCAR).

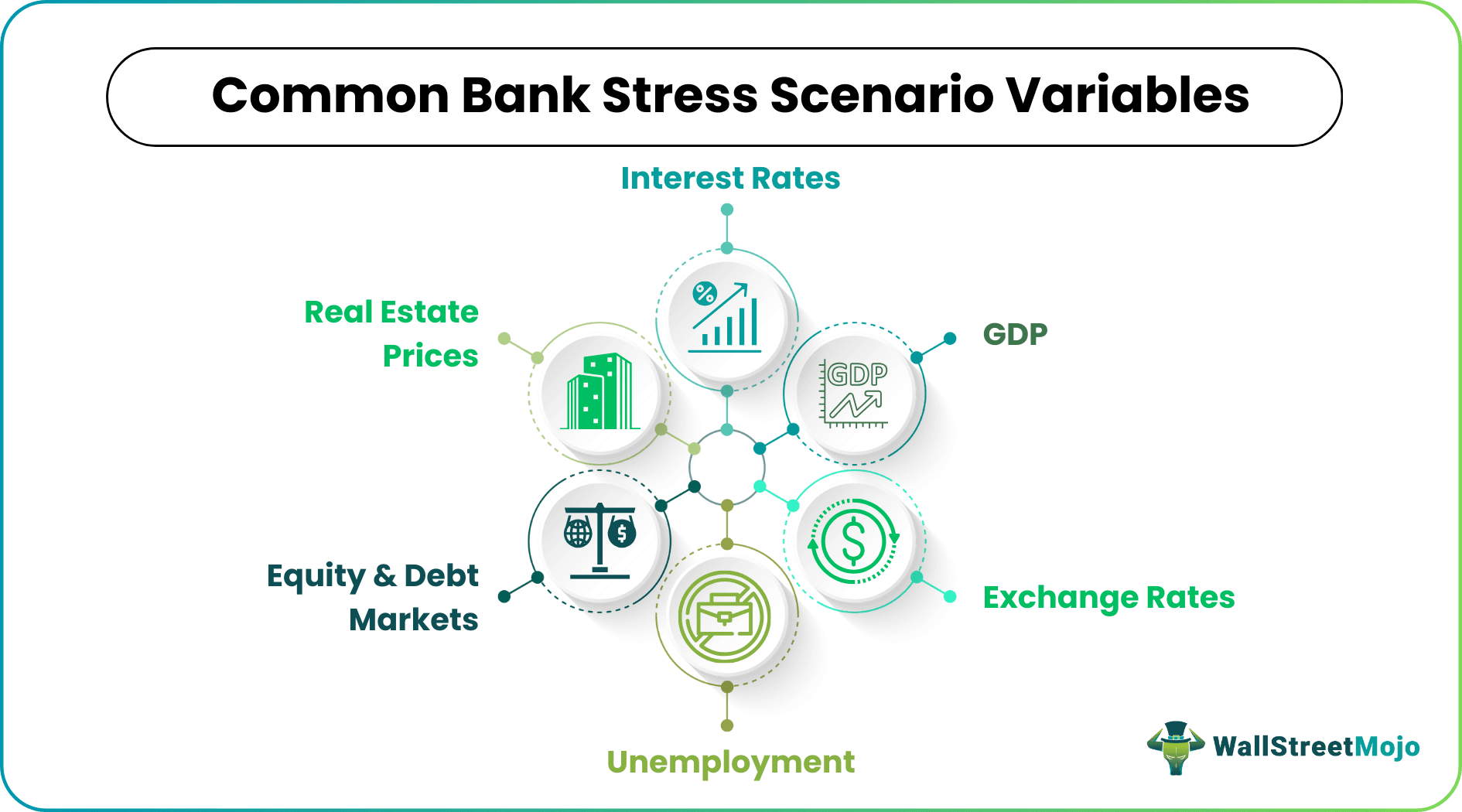

- The general variables used in the stress test are GDP, interest rate, unemployment, exchange rates, real estate price, and stock prices.

- Based on test result, regulatory agencies monitor and control bank's credit supply, share buybacks, and other actions.

How Does Bank Stress Test Work?

Bank stress tests are progressive. Generally, banks pass or fail the test based on the capital level analyzed during the economic downturn. If they can maintain minimum required capital during financial adversities, they get a pass in the stress test; otherwise, they fail. Failure in the trial will force them to limit certain activities like dividend distribution and share repurchases.

In the United States, the Federal Reserve accomplishes the stress test by completing two tests- the Dodd-Frank Act stress test (DFAST) and Comprehensive Capital Analysis & Review (CCAR). DFAST measures bank financial performance under hypothetical economic scenarios. CCAR analyses the proposed capital action plans for the upcoming four quarters prepared by the bank to measure the capacity of the bank to handle the impact of the economic downturn.

The stress test examines how financial institutions will thrive when people may not pay back loans or interests. The common hypothetical economic scenarios include economic shocks like recession and soaring unemployment. The typical stress scenario variables used in the test are GDP, interest rate, unemployment, exchange rates, real estate price, and stock prices. In addition, the test majorly focuses on credit risk, market risk, and liquidity risk.

According to the Federal Reserve, for the year 2014, the catastrophic scenario for DFAST consists of a massive recession with an unemployment rate of 11.25%, a GDP fall above 4%, a 50% collapse in the stock market, a 25% reduction in real estate values, and a roughly 35% drop in commercial real estate prices.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Bank Stress Test Example

Federal Reserve Stress Test 2021

The economic recession of 2007-2009 mandated the stress test to large banks in the United States. In the year 2021, the Federal Reserve released its annual bank stress test result 2021. A severe worldwide recession that affects commercial real estate and corporate loan holders, with 10.8% unemployment, results in a 55% loss in the stock market altogether forms the hypothetical economic scenario to run the test.

It is disclosed to the public that all 23 institutions maintained a minimum required capital levels during a hypothetical economic downturn even though they have a combined loss of $474 billion. Nevertheless, passing the test enabled them to resume and boost share buyback and dividend distribution to investors.

Advantages

- Transparency: Stress test discloses relevant information to investors and other consumers, mitigating future financial panic scenarios. Based on the stress test review, depositors can assess the institution's health and deposit in a healthy one.

- Guidance for preventive measures from regulatory bodies: Financial institutions that failed in the test are obliged to follow the restrictions set by regulatory bodies like decreasing the new issue of risky credit, dividend distribution, share repurchase, and overall credit card risk exposure annually. This prevents the banks from facing further economic and financial adversities. It also helps the banks in preserving capital.

- Improved risk management: It will save banks from the adverse impact of stock market bubbles. The test result shows banks their weakness and facilitates them to rectify the same and, in the process, avoid economic disaster.

- Situational policy updation: Banks can initiate alternate methods like lowering the interest rate, rewards to favor existing consumers in case of stall on credit facilities imposed by the government due to failure in the test.

- Systemic risk: Stress tests can reduce systemic risk, for instance, the risk faced due to Covid 19 pandemic scenarios.

Limitations

- Affects credit supply & cash flow: Various studies point out that bank stress tests may negatively affect credit conditions or credit supply affecting average consumers. Moreover, a decrease in cash flow affects the economic growth.

- The weak proportional relationship between result publication & stock returns: The equity market reacts to the stress test result depending on the economic scenario. For instance, a positive reaction to the result occurs when the economy is in crisis and vice versa.

- Lack of accurate solutions: The stress test result does not provide adequate or pinpoint solutions to deal with the adverse scenario.

- Variation of results: The simulation test result is not always in line with the actual case scenarios.

- Complexity: Stress testing may be challenging due to factors like cost and effort.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Ask Questions (FAQs)

The stress test assesses a bank's elasticity in response to different economic situations. It estimates whether the bank has the financial strength to survive economic downturns healthily.

In the United States, Federal Reserve System regulates the stress test. In Europe, the central regulatory bodies which govern the process are the Financial Services Authority (Stress and scenario testing CP08/24), Bank of England (Stress test Bank of England namely- Annual industry stress test), and European Banking Authority.

DFAST assesses the financial health of banks in the context of probable economic situations. For example, according to the Dodd-Frank Act Stress Test 2020, 33 Banks in the United States may suffer considerable losses if subjected to very unfavourable scenarios.

Recommended Articles

This has been a Guide to what is Bank Stress Test is and its Definition. Here we discuss how does bank stress test works along with an example, advantages, and limitations. You can learn more from the following articles –