Table Of Contents

What Is A Bank Holding Company?

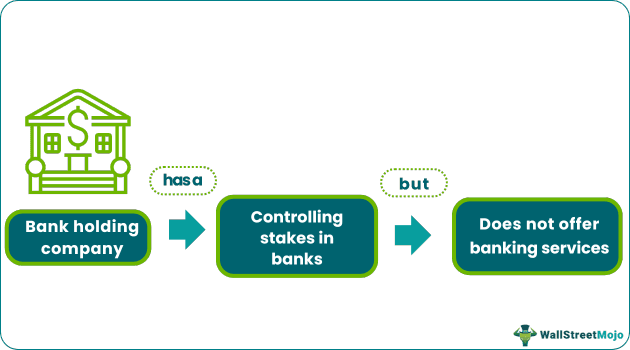

A bank holding company is a firm that has a controlling stake in one or many banks but doesn't directly engage in the offering of banking services. The banks owned by holding corporations are not managed on a day-to-day basis, but they have power over management and the organization's policies.

The adaptability of the bank holding company's organizational structure makes it possible to strengthen the capital position of the subsidiary bank. Additionally, it is advantageous as it permits more economic diversity than is possible when utilizing a bank.

Table of contents

- What Is A Bank Holding Company?

- A bank holding company is a business organization with a controlling stake in one or more financial institutions, such as banks.

- A holding company for one bank is referred to as a one-bank holding company. This holding company has been around for a shorter period and provides a more flexible structure for an independent bank.

- The ownership structure of a bank holding company accounts for ninety percent of all United States banks.

- Because it's a distinct legal entity from the banks it owns, it has greater autonomy in determining how its operations are carried out.

Bank Holding Company Explained

A bank holding company is any firm that satisfies even one of the two features: owns, administers, or has the authority to vote on at least 25 percent of a certain class of banking securities. In addition, maintains some degree of influence on the selection of the majority of a bank's governors or administrators in any capacity.

For a firm to qualify as a holding company, it is necessary to first receive approval from the Federal Reserve Board and then fulfill all of the prerequisites and conditions outlined in the Bank Holding Company Act and Regulation Y.

Forbidden activities for holding companies are trading and constraining holdings in hedge funds, venture capital, and related vehicles. However, for it to keep its business running, it may buy toxic assets, like investments that are difficult to sell, from a subsidiary bank. A holding company also issues debt. Subsidiary companies receive their proceeds for expansion.

When a parent issues debt and then contributes the proceeds to a subordinate bank as capital reserves, interest charges may be a cost that is tax deductible. As a result, the holding company can have a lower tax burden.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Regulations

- Federal Reserve Regulation Y governs bank holding companies and state-member bank procedures. In addition, regulation Y governs holding companies' minimum capital reserves, certain transactions, and the definition of nonbanking operations for bank holding companies operating in the U.S.

- The existence of "nonbank banks" operated by various financial firms allows them to completely avoid the act's regional, operation, and capital adequacy constraints. Money market funds made price controls outdated and eventually repealed them.

- The Douglas Amendment to the Act bars holding corporations from growing beyond state boundaries unless state legislation allows it.

- The Bank Holding Company Act requires clearance from the Governors of the Federal Reserve System for bank acquisitions. In addition, the Board must evaluate the holding firms' capital sufficiency.

Example

Let us consider an example to understand the concept better.

An article by Goldman Sach describes how they became a bank holding company. Goldman Sachs is a global investment bank and financial services firm based in the United States. It started in 1869, and its headquarters may be in Lower Manhattan. Goldman Sachs and Morgan Stanley, the final two big investment banks in the United States, said on September 21, 2008, that they would enter into regular bank holding companies.

This action reacted to the significantly altered scenario in marketplaces and the investment banking business driven by Lehman Brothers' failure and the subsequent global financial crisis.

As a holding company, Goldman Sachs will be eligible to use the discount window at the Federal Reserve, which is a secondary source of funding maintained by the Fed for financial firms that retain deposits. Having the status of a holding company would result in modifications to accounting rule standards and direct supervision from the Federal Reserve.

Bank Holding Company vs Financial Holding Company

- A bank holding company can issue loans, purchase hazardous assets, generate capital for subsidiary banks, minimize risk exposure, and qualify for tax benefits. In addition to what a holding company may do, financial holding companies can underwrite insurance policies, offer commercial banking services, and underwrite securities.

- A bank holding company can participate in nonbanking activities closely connected to banking. A financial holding company can conduct financial transactions

- A bank holding company has to declare itself as a Financial holding company to get that status, whereas a financial holding company is already a bank holding company.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

The banks owned by holding corporations are not managed daily by those holding companies. But on the other hand, they have power over management and the organization's policies.

A type of financial organization that focuses largely on providing residential mortgage loans and receives deposits from individual customers as its primary source of financing. A firm that influences another savings association holding company or the other saving and lending holding company, either directly or indirectly. Any firm, also a holding company, is not eligible for this incentive.

Nonbank subsidiaries are businesses owned by bank holding firms that provide nonbank products and services, such as insurance and investment advice. Still, they do not offer banking products that the Federal Deposit Insurance Corporation insures, such as checking and savings accounts. Some examples of nonbank services and goods include healthcare and financial advice.

Recommended Articles

This article has been a guide to What is Bank Holding Company. We explain its regulations, an example, and compare it with a financial holding company. You can also go through our recommended articles on corporate finance -