Table Of Contents

Bank Credit Meaning

Bank credit is usually referred to as a loan given for business requirements or personal needs to its customers, with or without a guarantee or collateral, with an expectation of earning periodic interest on the loan amount. The principal amount is refunded at the end of loan tenure, duly agreed upon, and mentioned in the loan covenant.

In today’s world, demands are continuously increasing, but the means to fulfill those demands are limited; hence borrowing money will enable financing the varied needs of a business, profession, and personal. Depending on the type of loan and the agreement on the bank credit letter, these loans are either instalment-based, open credit, or revolving credit.

Table of contents

- Bank Credit Meaning

- Bank credit typically refers to loans provided to customers for personal or business purposes, with or without collateral, intending to regularly earn interest on the principal.

- Secured loans are backed by collateral, which serves as a guarantee to the bank. Collateral can include property, debtors, stock, fixed deposits, or any other asset the bank can sell or liquidate if the borrower fails to make installment payments.

- Working capital loans are obtained when businesses struggle to manage their working capital effectively.

Bank Credit Explained

Bank credit refers to the loan extended to fulfil business needs without any collateral or security being provided. Similar loans are extended to individuals through bank credit cards, however, for business, loans are provided on a particular interest rate that is repaid through instalments, through open or revolving credit.

Bank credit helps an organization meet business needs; however, there should be the right mix of debt and equity components to have healthy financial statements.

This credit is given to borrowers to fulfill the necessary documentation required by the Bank. Interest rates and repayment terms are duly mentioned in the loan covenant. Documentation to the Bank includes:

- Financial statements.

- Income tax returns.

- Projected financial statements for three to five years.

- Changes are based on the type of loan and from person to person.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

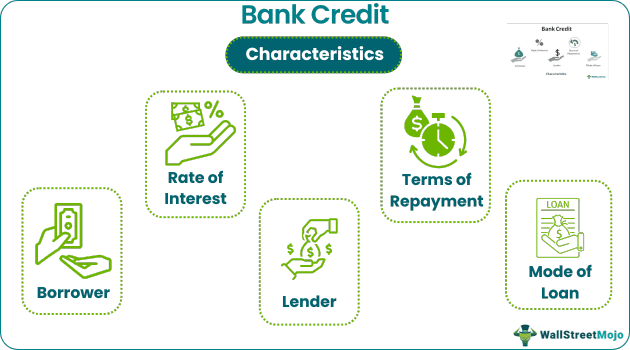

Characteristics

Multiple individuals and organizations come together before a bank credit letter is issued. Let us understand the parties involved and their characteristics through the discussion below.

- Borrower: A person who borrows money.

- Lender: The person who lends money is usually the bank.

- Rate of Interest: The interest rate can be a fixed or floating rate of interest. The floating interest rate is based on benchmark rates like LIBOR or MIBOR.

- Terms of Repayment: These are mentioned in the loan covenant and strictly adhere to avoid the prepayment penalty.

- Mode of Loan: Normally given in cash but sometimes will be given in the form of raw material or fixed assets.

#1 - Classification Based on Borrower

Let’s discuss classification based on the borrower.

#1 - Loan for Personal Purpose

Personal loans are given to meet the particular needs of the group and individual. For example, personal loans are taken to purchase consumer goods, electronics, houses, vehicles, etc.

#2 - Loan for Business or Profession Purposes

These loans are offered to meet the needs of the business. It can be a working capital loan or cash credit facility to meet a short-term liquidity crunch. Companies borrow money for major fixed asset expansion, business diversification into different product portfolios, and varied customer segments. The purpose of lending money will be different for different businesses based on circumstances, needs, and environments in which the company operates.

#2 - Classification Based on Security

Let’s discuss classification based on security.

#1 - Secured Loan

Secured loans are secured against collateral, a guarantee given to the Bank by the third party. Loans can be secured against property, plant and machinery and equipment, debtors, stock, fixed deposits, and any other asset which can be sold or liquidated by the Bank in case of nonpayment of installment on the part of the borrower.

Bank will also lend money against the guarantee given by the third party on behalf of the borrower. In the case of a guarantee, the guarantor will be liable to pay a balanced amount if the borrower fails to do so.

#2 - Unsecured Loan

Unsecured loans are neither secured against any asset nor any guarantee is provided to the Bank. A borrower with a great history of the settlement of dues, good credit rating, and sound financial records will generally get an unsecured loan. Unsecured loans are usually provided by small banks, ‘Patpedhies,’ and relatives.

#3 - Classification Based on Duration

Let’s discuss classification based on the duration.

#1- Short Term Loans

These loans are given for a shorter duration, say one month to one year.

- Credit Card Loans: These usually are given for one month. The Bank issues credit cards to borrowers to facilitate the day-to-day needs of businesses and individuals. Credit cards are issued to sales managers with a specific limit to spend expenditure on travel and sales-related expenses. Individuals use credit cards for day-to-day requirements.

- Cash Credit Facility or Bank Overdraft Facility: This is extended to current account holders to withdraw more than the debit balance of the bank account. CC or bank OD facility is mainly used when a business has a cash crunch and must settle sudden liabilities.

- Working Capital Loans: These can be short-term or long-term in nature. It depends on the working capital cycle of the company. The working capital cycle may be more than twelve months in an industry that sells seasonal goods. A working capital loan is required when companies cannot manage working capital effectively. The credit period allowed by vendors is lower than the credit period allowed to debtors, and the stock turnover ratio is higher when the need for working capital loans arises. The Stock turnover ratio means how quickly businesses can convert stock into sales.

#2 - Long Term Loans

These loans are given for longer, say three to five years or more than that. These loans are provided for the expansion of business, diversification of product portfolio or business, substantial investment in fixed assets, and real estate where the cost to buy such assets or investments is so vast that repayment of the same within a year is not possible.

Purpose

Despite the wide array of loans provided by banks which include conventional mortgages or loans, and bank credit cards, these loans are attractive for businesses for more than one reason. Let us understand the purpose of banks issuing these loans and businesses preferring them over other possible options through the explanation below.

- Educational Loans: These are given for pursuing higher education, repayment of which is due after completing education. Interest gets accumulated for the loan.

- Housing Loans: These are given to buy a home. The repayment of principal and interest is based on the EMI principal. House is collateral for such loans, and excessive documentation is required.

- Vehicle Loans: These are given to purchase vehicles like cars, tempo, two-wheeler, autos, and trucks. Normally assets are hypothecated to the Bank unless and until the final installment is paid. You often see “we banked …. Bank” written on the backside of cars. This indicates a loan is taken from “… Bank”.

- Vendor Financing: This is an arrangement provided by the Bank to pay to vendors as per agreed credit terms, and in turn, the borrower will pay to the Bank after, say, 60 days or 90 days. The Bank charges an interest rate to the borrower for paying in advance to suppliers. The advantage of this is minimal documentation required by the Bank.

- Letter of Credit Facility: Like vendor financing but predominantly used while importing goods or making payments to overseas vendors. Terms of repayment and interest rate are mutually agreed upon between the parties.

Advantages

Let us understand the advantages of securing a bank credit letter through the points below.

- The loan is not repayable on demand. Terms of repayment and interest rate are pre-decided; hence, cashflows can be managed better.

- It helps businesses and individuals when there is a need for funds.

- Interest payments can be negotiated and paid only for a certain period, and during the balance, the borrower will pay only the principal.

- The cost of debt is lower than the cost of equity; hence the appropriate proportion of debt in the portfolio enhances returns to equity shareholders by leveraging the cost of debt.

Disadvantages

Despite the various advantages mentioned above, there are a few factors that prove to be a hassle or hurdle in securing the finance required. Let us understand why in some cases a bank credit card might be a better option than this form of a loan through the discussion below.

- A borrower may have to surrender ownership of an asset if installments are not paid in time.

- Bank charges one-time processing fees that need to be paid upfront.

- There is a prepayment penalty if the borrower pays the loan in advance.

- Companies should maintain the right debt-equity ratio. If there is a significant reliance on loans by the Companies, it will be difficult to pay interest in the event of a crisis.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

The function of bank credit is to provide loans or credit to customers for various purposes, such as personal expenses or business investments. Banks extend credit to individuals and businesses to meet their financial needs and support economic growth. By granting loans, banks earn interest income and facilitate economic activities by providing access to funds that individuals and businesses may not have immediately available.

Bank credit risk refers to the potential for borrowers to default on their loan repayments, leading to financial losses for the bank. It arises from the uncertainty of whether borrowers will fulfill their contractual obligations, including paying interest and principal amounts on time.

A bank credit analyst is a professional responsible for assessing the creditworthiness of borrowers and analyzing the risks associated with extending credit. They evaluate loan applications, review financial statements, analyze market trends, and assess various risk factors to determine the probability of repayment. Bank credit analysts play a crucial role in making informed lending decisions, managing credit portfolios, and ensuring the bank's overall financial health and stability.

Recommended Articles

This has been a guide to Bank Credit & its meaning. We discuss its purpose, characteristics, classification based on borrower, security, and duration. You can learn more about finance from the following articles –