Table Of Contents

Bail-in Meaning

A bail-in is a facility that provides relief to a financial institution such as a bank by canceling some of the debt it owes its borrowers. This measure is taken when the institution is struggling with debt and is on the verge of failure. The point of the bail-in is to save the bank from falling into bankruptcy.

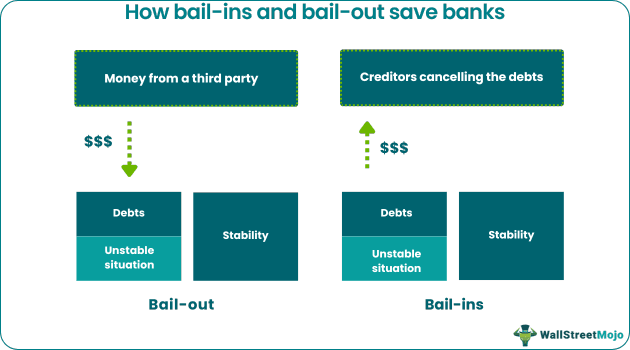

Thus a bail-in helps a financially weak institution to survive and keep working. Bail-ins are an alternative to bail-outs, another rescue mechanism where a third party like the government infuses the taxpayer's money into the institution under stress to ease their debts. However, unlike bail-outs, in the case of bail-ins creditors bear the burden of loss.

Table of contents

- Bail-in Meaning

- A bail-in is a form of debt management for a large firm or financial institution, where the debt is commonly canceled or restructured to keep the company afloat.

- Unlike bail-outs, where a third party funds money to help the institution pay off their debts, bail-ins force the creditors to write off or restructure the debts to stabilize the firm.

- While the bail-out makes taxpayers face all the burden, bail-ins shift that responsibility to the creditors.

- Negotiations regarding a bail-in agreement are usually brokered by the SEC or a firm given the task to do the same.

- The solution to the Cypriot banking crisis with the German pitch-in is one of the most famous cases of famous bail-ins in history.

How Does Bail-in Work?

Bail-in strategies help a financial institution avoid its collapse. The downfall of such an institution can leave serious aftermaths in the economy and may affect other markets. There are several ways out for a distressed financial institution, and bail-in is one of the most popular methods. In the recent past, financial institutions, many businesses like airlines affected by the Covid-19 pandemic had to use a bail-in to try and stem the risk of collapse.

In a bail-in, the institution or the firm can have their debts to the creditors canceled. It gives the institution more room to maneuver and keep operating. Many companies providing bail-in services require the institution to make sacrifices, such as reducing their workforce or taking other austerity measures. This is to minimize any unnecessary expense that the company would have to shoulder. An institution in financial straits has to get rid of all its excess expenses. In addition to that, some bail-in companies may even want to change the institution's boards of directors if increases the profits in the long run.

The bail-in firm comes in to reduce the chances of dissolving a firm forever and help it grow back to its former position. By writing off or restructuring the debts, the firm can stabilize itself. And the economy does not have to endure painful shifts of an institutional collapse.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Bail-in vs Bail-Out

It is easy to confuse a bail-in and bail-out. In the 2008 financial crisis, the US government lent money to some firms (with strict conditions) so that they are not lost to debtors. In this case, they used the money to sort out the firms' needs to keep them afloat. This is an example of a bail-out. In a bail-in, a company or other firm in financial trouble has to report this to the authorities. The creditors to the firm bear some of the financial fallout, either by canceling some or all the debt. They can also come with a plan on how the debtors would make payments, or even turn some of the debt into ownership of the company by converting them into shares. An agreement brokered by the SEC is the way to do this.

Real World Examples

The Cypriot banking crisis

A real-world example of bail-in is the Cypriot banking crisis in Europe. The Central Bank of Cyprus was experiencing a financial crisis and was on the edge of collapse. However, Germany came to their aid, providing funds that could cancel the debts of any debtors. This would allow the bank to flourish. In addition to this, the bank also had to take several measures to stay afloat. One of these was to have the Cypriot bank levy only one tax on bank deposits. This step alone raised around $7.5 billion. The German bank saving the Cypriot central bank meant that more people would be confident in using the bank services. This way the deposits would increase. By taxing any bank deposits, the bank would raise a lot of money. They could use some of this money to pay back the German government.

How bail-ins saved the Cypriot bank

The bank's failure had resulted in losses for the people who had money in the bank. To alleviate this, the German government demanded the bank to give each depositor stock in the bank equal to the value of the money they lost during the duration. This way, the bank would not need to pay out money when people decided to withdraw it (which the bank did not have). It would also help the banking system retain its value and reputation.

The goals of the bail-in for the Cypriot bank were to ensure that it had liquidity, reduce the pressure from creditors and give a cash injection that would allow all the banks to keep operating. But, more importantly, it would also keep people having faith in their banking system so that more and more would deposit. This then would make the Cypriot banks more liquid

Bail-ins and European commission

In May 2015, the European Commission issued a fresh set of guidelines for bailing the failed banks. That year, EC asked 11 countries to adopt new rules touching on this issue. They had to do this within two months or face legal measures. France and Italy were among the countries that were expected to abide by the new regulations. These regulations came to be called Bank Recovery and Resolution Directive (BRRD). The primary objective of BRRD was to protect taxpayers from bailing troubled lenders. Instead, under the new rules, shareholders and creditors have to now chip in to rescue these troubled institutions through "bail-ins."

When Italy faced a banking crisis in 2016, authorities considered bail-ins as a viable option for getting the banks out of trouble. However, they ultimately decided against such a move due to a couple of reasons. First, the question of morality outweighed any gains the country or any of its banks stood to enjoy. Secondly, Italy's banking sector was teeming with many weaknesses that made such a solution seem unwise, untimely, and unattractive. Those weaknesses made it uncomfortable for the authorities to use taxpayers' money to help the failing banks.

Bail-in laws

In the United States, the constitution did not clearly define bail-in and bail-out laws until the 2008 financial crisis. The use of bail-outs as a rescue strategy for organizations deemed "too big to fail" invited widespread public discontent. It led the government to pass the consumer act of January 10, which encourages the replacement of bail-outs with bail-ins. The Dodd frank bail-in reforms gave new responsibilities to the Federal deposit insurance corporation(FDIC). The FDIC now protects the depositors by insuring bank accounts for a maximum of $250,000. The Dodd-Frank bail-in act put forth sufficient similar reforms to protect taxpayers from carrying the load of bail-outs. These reforms were able to reduce bail-outs by enabling more bail-ins.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

A bail-in clause forces the creditors of a financial institution like a bank to write off or cancel some of its debts. It is done to protect the struggling institution from collapsing itself and causing economic repercussions.

A bail-in clause is used when an institution like a bank is under obvious financial distress and is on the verge of failing. The bail-in aims to save the bank from potential collapse and keep operating so that it can come back to its former glory.

A bail-out happens when a powerful third party like the government helps a struggling financial institution pay its debts by injecting money into it. This is usually the taxpayers' money, and they will have to carry the burden of saving the banks. But in a bail-in, the creditors are forced to carry this burden as they are made to cancel the debts or restructure them in some way under several conditions.

Recommended Articles

This has been a guide to Bail-in and its meaning. Here we discuss how bail-ins work along with examples and laws. We also discuss the difference between Bail-in and Bail-out. You may learn more about financing from the following articles -