Table Of Contents

What Is Asset-Based Valuation?

Asset-based valuation refers to one of the approaches used to calculate the value of a business. It values a business based on the assets it possesses. The method evaluates assets and liabilities, obtains their fair market value, and deducts the liabilities from assets.

The method is an effective way to determine the price demandable while selling a company. In addition, it helps analyze the cost of recreating a similar business or replacing all assets per the current market environment. Hence, clear information about the business's worth helps the owner confidently make deals and offerings.

Key Takeaways

- An asset-based valuation approach determines the fair market value of all assets to determine the current worth of the firm. The method is important because assets are an important factor in the revenue generation process.

- The common valuation methods are asset accumulation and the excess earning valuation method.

- The pros of the method are flexibility, simplicity of the formulas used, the inclusion of off-balance-sheet items, etc.

- The cons are complexity in valuing intangible assets, disregarding earnings in the calculation, assets do not necessarily point to the profitability of an entity, etc.

Asset-Based Valuation Explained

Asset-based valuation model derives the value of a company by determining the fair market value of its assets. Assets are an important factor in revenue generation. Every company with active business and operations has a set of assets and liabilities. Assets can be tangibles like property, plant & equipment (PPE) or intangibles like copyrights and trademarks.

The basic concept implies that the value of the total company equity is equivalent to the value of the total company assets (tangible and intangible) minus the value of the total company liabilities (recorded and contingent). An analyst can use different techniques to value an asset. For example, they can follow balance sheet values, replacement values, or fair market values.

It is a generally accepted business valuation method. The method is flexible and complex at the same time. The provision to add off-balance-sheet items like contingent assets or liabilities explains its flexibility. The market worth of tangible assets is easily estimated using book value. However, estimating the value of intangible assets makes the method complex. As a result, this method may necessitate more data, analyst effort, and associated expenditures than alternative valuation approaches.

Asset-Based Valuation Methods

Let's discuss two famous methods of valuation: the asset accumulation method and the excess earning valuation method.

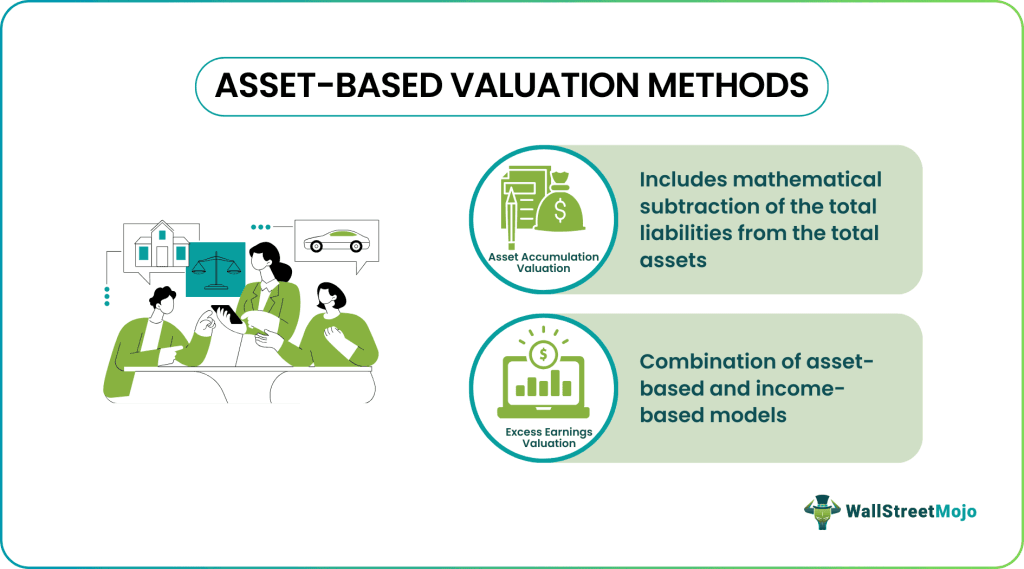

#1 - Asset Accumulation Valuation

The asset accumulation valuations methods resemble the balance sheet equation; that is, the difference between the value of assets and liabilities gives the company's equity value or net worth. The method considers all the assets and liabilities, even the items not present on the balance sheet. For example, it includes the values of intangible assets like trademarks and contingent liabilities, which usually appear in the footnotes to the financial statements.

#2 - Excess Earnings Valuation

Excess earnings valuation method recommended by IRS Rev. Rul. 68–609 combines asset-based and income-based models aggregating asset and income information. The IRS ruling also states that the technique "should not be used if there is better evidence available from which the value of intangibles can be determined." The method uses two capitalization rates to identify tangible vs. intangible assets returns. So, a combination of the tangible and intangible asset values contributes to evaluating the company's overall value.

Various studies suggest that the excess earnings method is a feasible valuation alternative for privately held firms, lacking analyst monitoring. The difficulty in estimating two capitalization rates, on the other hand, acts as a disincentive to broader usage in business valuation.

Examples

To find the value using an asset-based approach, an analyst start this valuation procedure with an audited balance sheet. All entity assets and liability accounts are subject to revaluation to the valuation assignment standard of value. To prepare a revalued balance sheet, the analyst identifies and capitalizes all of the entity's assets and liabilities. This process includes all of the assets and liabilities that are already recorded on the entity's balance sheet and not recorded on the entity's balance sheet.

Based on the values in the revalued balance sheet in line with the fair market value:

- Total assets: $107 billion

- Total liabilities: $60 billion

- Value: Total assets – Total liabilities = $107 - $60 = $47 billion

Consider another asset-based valuation example where the book value of assets is $50,000 (current assets, fixed assets, and other assets like investment in subsidiaries); the corresponding total derived after adding the fair market value of each item in the asset list is $76,000. The fair market value of intangible assets is $10,000. So, the value of the total assets is $86,000. The book value or fair market value of current and long-term liabilities is $33,000. In the next step, add $7,000 as the value of contingent liabilities; the total liabilities are $40,000. Finally, the total owner's equity is derived by deducting liabilities from assets, $46,000.

Pros And Cons

Pros

- It is the most preferred method in a critical context like liquidation and M&A.

- It follows simple mathematical formulas.

- Consider off-balance-sheet items.

Cons

- Having innumerable assets does not point to the profitability of the business.

- Valuing the intangible assets requires attention to detail and making the overall process complex.

- The method does not include the earnings of the company.

- Requires revaluation to derive the fair market value.