Table Of Contents

What Is An Amortization Table?

The amortization table reflects the schedule of periodic payments to be made with respect to a loan undertaken, representing the principal amount and the interest amount payable in each periodic installment. Thus, it is a detailed working of the loan repayment, containing particulars of equated installments, its principal portion, and the interest portion for each installment until the loan is repaid.

The amortization table schedule is a financial tool of utmost significance, providing a systematic breakdown of loan repayments over time. It empowers borrowers and lenders with a clear roadmap, delineating how each payment contributes to principal and interest. This transparency fosters financial planning, aiding borrowers in understanding their obligations and lenders in assessing the financial dynamics of the loan portfolio.

Table of contents

Amortization Table Explained

An amortization table is a repayment schedule for any loan. It reflects the total number of installments that are to be made for full amortization, i.e., the entire repayment of the loan. The loan amortization schedule reflects the monthly installment and the breakup of principal repayment and interest in each installment. Although the monthly installment will be the same for each month, the separation of principal repayment and interest will be different for each month because the loan outstanding will differ each month. By referring to this table, a person can be aware of future payments and the due loan amount.

The amortization table chart serves as a strategic financial guide for borrowers, outlining the trajectory of their loan repayment. It offers a month-by-month or period-by-period breakdown, revealing the diminishing interest and increasing principal components with each installment. This transparency empowers borrowers to comprehend the financial implications of their payments, aiding in budgeting and long-term financial planning.

For lenders, the amortization table is an invaluable tool for risk assessment and financial management. It allows them to gauge the evolving risk associated with the loan as the balance between principal and interest shifts over time.

Therefore, the amortization table serves as a financial compass, guiding both borrowers and lenders through the intricacies of loan repayment dynamics. Its significance lies in fostering financial literacy, facilitating prudent decision-making, and promoting a transparent understanding of the evolving financial relationship between borrowers and lenders.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Characteristics

An amortization table schedule works best for the following kinds of loans.

- The loan disbursement is done as a lump-sum amount.

- The loan has to be repaid over a while in monthly installments.

- The installment that is paid each month is of equal amount, known as equated installment.

- The rate of interest that is being applied to the loan is fixed.

How to Calculate?

The interest portion reflected in the amortization table is calculated by multiplying the outstanding opening principal by the monthly rate of interest. The monthly rate of interest can be calculated by dividing the yearly rate of interest by twelve. The outstanding principal is always mentioned in the amortization schedule. As the exceptional principal keeps on decreasing with each monthly repayment, the interest portion will also fall.

Example

Let us understand the practical application of the amortization table chart through the example below.

- Loan Amount = $1,00,000

- Interest Rate = 12% P.A.

- Tenure = 24 Months

- Loan Date = 01.01.2019

The amortization for the above loans looks like below.

The amount of EMI payable per month is $4,614, and the tenure of the loan is 24 months.

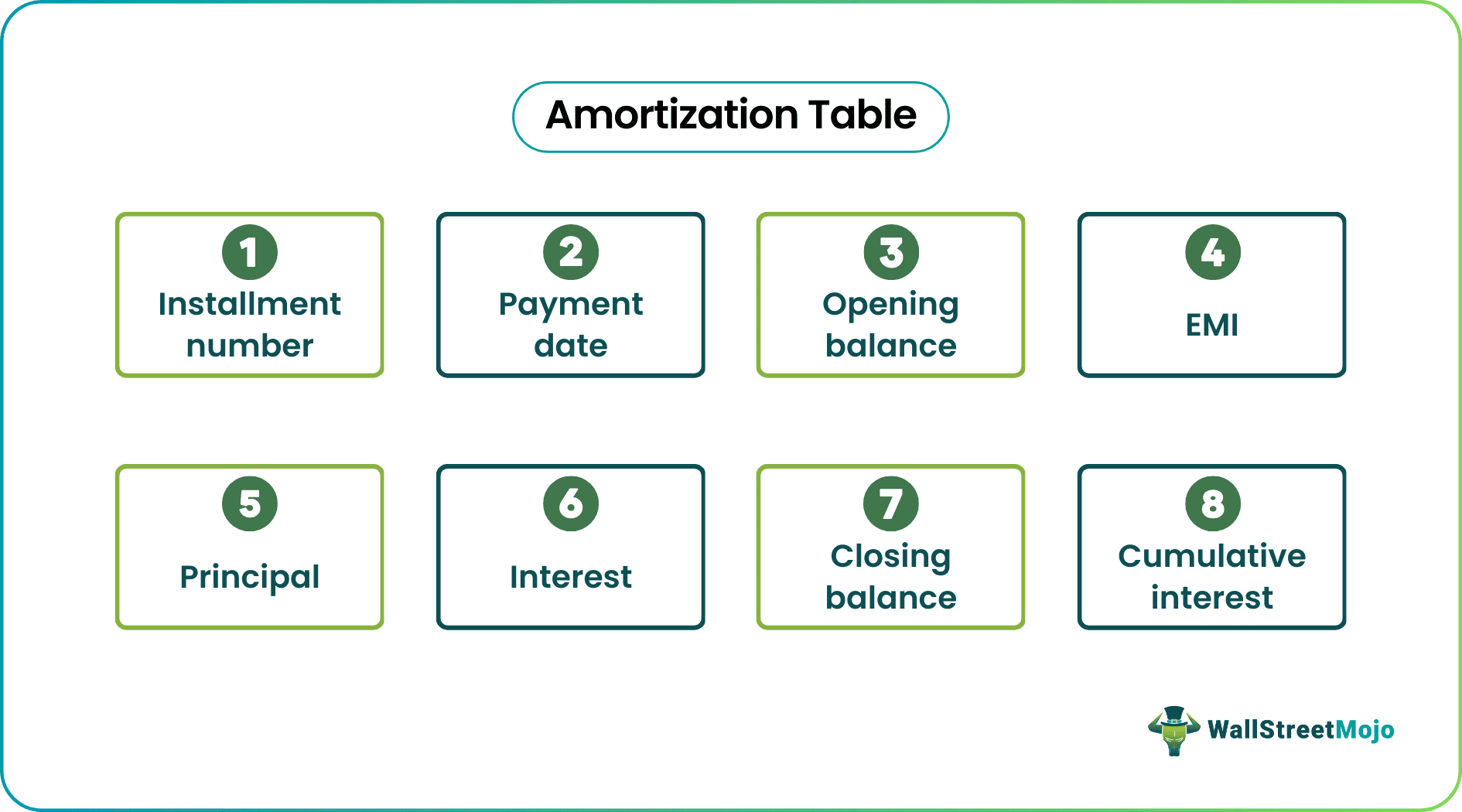

What Does It Show?

A table, as presented above, shows the following particulars.

- Installment Number: It reflects the wise serial number of installments. The last installment number represents the tenure of the loan.

- Payment Date: It means the date on which the payments are due each month.

- Opening Balance: It reflects the opening balance of the outstanding principal of the loan.

- EMI: It means the fixed amount of payment that is to be done each month.

- Principal: In this column, the principal amount out of the EMI amount due is being reflected.

- Interest: This represents the interest portion out of the EMI amount due.

- Closing Balance: Closing balance means the closing balance of the principal amount of loan after the repayment of the current month.

- Cumulative Interest: It reflects the total amount of interest that has been incurred on loan at each installment level.

How to Use the Amortization Table?

This table is used to calculate certain factors such as the EMI amount and the total interest cost involved in forgiven loan amount at the given rate of interest for a fixed tenure. The table will provide exact details of the same, and the borrower can ascertain the effect of the same on his financials. The same is also helpful in keeping track of the upcoming loan repayments.

Amortization Table vs. Payment Schedule

While both these terms might seem similar in function and applicability, there are differences in their fundamentals and implications. Let us understand the differences between amortization table schedule and payment schedule through the comparison below.

Amortization Table

- Presents a detailed breakdown of each loan payment, specifying the portion allocated to principal and interest.

- Includes information on the outstanding loan balance, cumulative interest paid, and the impact of each payment on the loan's overall structure.

- It offers a dynamic view of the loan's lifecycle, revealing the changing ratio of principal and interest with each installment.

- Empowers borrowers with a comprehensive understanding of their repayment journey, aiding in financial planning and budgeting.

- It enables lenders to assess the evolving risk associated with the loan and adapt strategies accordingly.

Payment Schedule

- Provides a broader overview, outlining the timing and amount of each scheduled payment throughout the loan term.

- Typically includes due dates, payment amounts, and the cumulative total paid at specific intervals.

- It serves as a static document, specifying when payments are due without delving into the specific allocation between principal and interest.

- Also, it offers a straightforward timeline for borrowers to follow, emphasizing due dates and total amounts payable at each period.

- Provides a basic overview of cash flow expectations but lacks a detailed breakdown of how payments impact the loan's composition.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Recommended Articles

This has been a guide to what is an Amortization Table. Here we explain its characteristics, how to use, example, and compare it with repayment schedule. You can learn more about financing from the following articles –