Table Of Contents

What Is The Amortization of Bond Premium?

Amortization of Bond Premium refers to the amortization of excess premium paid over and above the face value of the Bond. A bond has a stated coupon rate of interest and pays interest to the bond investors based on such a coupon rate of interest. It is valued at the present value of interest payments and face value determined based on the market interest rate. The investors pay more than the face value of the bonds when the stated interest rate (also called coupon rate) exceeds the market interest rate.

- When a bond is issued at a price higher than its face value, the difference is called Bond Premium. The issuer has to amortize the Bond premium over the life of the Bond, which, in turn, reduces the amount charged to interest expense. In other words, amortization is an accounting technique to adjust bond premiums over the bond's life.

- Generally, bond market values move inversely to interest rates. When interest rates go up, the market value of bonds goes down and vice versa. It leads to market premiums and discounts on the face value of bonds. The bond premium has to be amortized periodically, thus reducing the cost basis of bonds.

Methods of Amortization of Bond Premium Calculation

Premium Bond Amortization can be calculated based on two methods, namely,

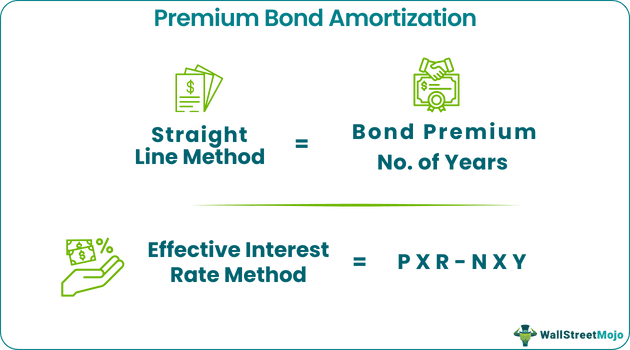

#1 - Straight Line Method

Under the straight-line method, the bond premium is amortized equally in each period. It reduces the premium amount equally over the life of the bond. The formula for calculating the periodic amortization under the straight-line method is:

Bond Premium Amortized = Bond Premium / No. of Years

Example of Premium Bond Amortization

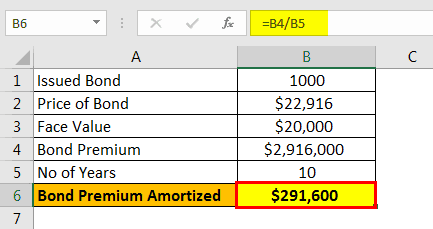

Let us consider if 1000 bonds are issued for $ 22,916, having a face value of $20,000.

The Bond Premium will be

Bond Premium = $2916000

Bond Premium Amortized calculation can be done using the above formula as,

=($22,916 - $ 20,000) X 1000

Bond Premium Amortized will be -

Bond Premium Amortized =$ 291,600

Therefore, the Bond Premium amortized will be $ 2,916,000/10 = $ 291,600

#2 - Effective Interest Rate Method

Under the Effective Interest Rate Method, amortization is done by reducing the balance in the premium on bonds payable the difference between two terms or periods. Under this method, the bond premium to be amortized periodically is calculated by using the following formula:

Bond Premium Amortized= P x R – N x Y

Where,

- P = Bond issue price,

- R = Market Rate of interest,

- N = Nominal or face value and,

- Y = coupon rate of interest/ Yield

Example of Premium Bond Amortization

Let us consider an investor that purchased a bond for $20,500. The bond's maturity period is 10 years, and the face value is $20,000. The coupon rate of interest is 10% and has a market rate of interest at 8%.

Let us calculate the amortization for the first, second, and third period based on the figures given above:

For the remaining 7 periods, we can use the same structure presented above to calculate the amortizable bond premium. It can be seen from the above example that a bond purchased at a premium has a negative accrual, or in other words, the basis of the bond amortizes.

The accounting treatment for Interest paid and bond premium amortized will remain the same, irrespective of the method used for amortization.

The journal entry for interest payment and bond premium amortized will be:

Advantages and Limitations

The primary advantage of premium bond amortization is that it is a tax deduction in the current tax year. Suppose the interest paid on the bond is taxable. In that case, the premium paid on the bond can be amortized, or in other words, a part of the premium can be utilized towards reducing the amount of taxable income. Also, it leads to reducing the cost basis of the taxable bond for premium amortized in each period.

However, in the case of tax-exempt bonds, the amortized premium is not deductible while determining the taxable income. But the bond premium has to be amortized for each period, and a reduction of cost basis in the bond is necessary each year.

Conclusion

For a Bond investor, the premium paid for a bond represents part of the cost basis for tax purposes. Therefore, premium amortized yearly can be used to adjust or reduce tax liability created by interest income generated from such bonds.

Calculating Bond Premium amortized can be done by any of the two methods mentioned above, depending on the type of bond. Both bond amortization methods give the same final results. However, the difference arises in the pace of interest expenses. The Straight Line method of amortizationgives the same interest expenses in each period.

An effective Interest rate method of amortization, on the other hand, gives decreasing interest expenses over time for premium bonds. In simple words, expenses decrease with a decrease in book value under the Effective Interest rate method. This logic seems practical, but the straight-line method is easier to calculate. If the primary consideration is to defer current income, the Effective Interest rate method should be chosen to amortize the premium on bonds. The Straight Method is preferable when the premium amount is very less or insignificant.