Table Of Contents

Alternative Trading System Definition

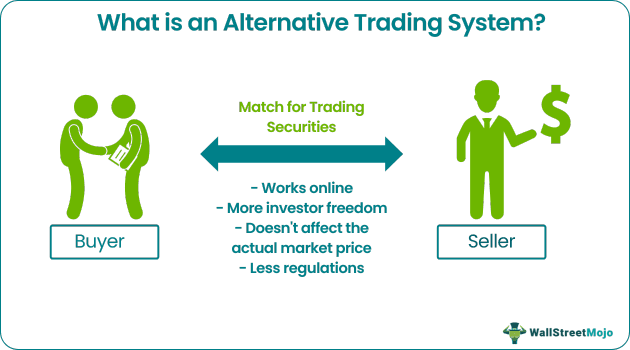

An alternative trading system (ATS) is a trading platform or venue resembling a stock exchange where orders are matched for buyers and sellers. However, an ATS is less regulated by the Securities and Exchange Commission (SEC) than an exchange. Most ATSs bring together buyers and sellers of securities through an electronic medium.

Also known as multilateral trading facilities, ATSs do not employ strict rules and regulations for their subscribers. Further, it allows the investors to buy and sell without disclosing the details of their investment, thereby facilitating institutional investors to trade large securities without affecting the market prices of securities.

Key Takeaways

- An alternative trading system (ATS), like an exchange, allows investors to invest in securities. It functions by matching buyers and sellers registered.

- But unlike a national exchange, such as the NYSE or NASDAQ, the SEC does not regulate the ATS heavily.

- As the term implies, the ATS is an alternative mode for trading rather than an exchange.

- Amid criticisms over the operations of an ATS, the SEC began publishing the alternative trading system list in 2009 as part of a move to make the ATS more transparent.

Alternative Trading System Explained

Alternative trading system companies have become popular and accepted over the years, owing to how they operate and their advantages, especially to investors.

Firstly, ATS is not regulated strictly like a stock exchange. Secondly, ATS does not establish rules for the investors and trading securities, i.e., it is not self-regulatory. Thirdly, it provides an option for institutional investors to buy or sell in large quantities. Lastly, investors can trade on an ATS without disclosing investment size or price information.

Though there is a huge public criticism concerning the functions of an ATS, like lack of transparency, unethical use of investor information and data, public non-disclosure, etc., ATS is legal but loosely regulated.

However, less regulation does not correlate with an absence of regulation. For example, the SEC Regulation ATS oversees the function and operation of an ATS. Also, recently the SEC has been taking many measures to make the ATS more transparent, following heavy criticism. For example, the SEC publishes the alternative trading system list monthly on its website. Further, it has mandated that the ATS should report records and other relevant information.

To become an ATS, an entity should register as a broker-dealer under Exchange Act Rule 3a1-1(a). Also, it should comply with regulation ATS rules 300-303. Though initially not registered as an exchange, alternative trading system companies can later apply to the SEC to become a national exchange.

Many traders use Saxo Bank International to research and invest in stocks across different markets. Its features like SAXO Stocks offer access to a wide range of global equities for investors.

Examples

Consider the following examples of ATS and their characteristics:

#1 - Electronic Communication Networks

Electronic communication networks (ECN) facilitate online trading. Investors can buy and sell even in non-trading hours without needing a broker. Thus, it is flexible. ECN automatically matches buyers and sellers and charges the fees or commission when transactions occur. It also breaks geographical barriers as it works online.

#2 - Dark Pools

The dark pool alternative transaction system is the most prominent ATS type. It permits traders to stay anonymous while performing transactions. Traders prefer the dark pool alternative transaction system due to the lack of regulations, which give them absolute freedom in the trading venue. Dark pools are also used by investors who do not want their buying or selling decisions to affect the stock or the market.

#3 - Crossing Networks

The crossing network ATS is similar to the dark pool considering the transparency and confidentiality of the market. However, in a crossing network, the stocks and securities are traded only via ATS and not through an exchange. Trading securities exclusively in an ATS is referred to as crossing networks.

#4 - Call Markets

In a call market, trading doesn’t occur continuously but at regular intervals or when the price reaches the expected price or the clearing price. This price is determined by considering the securities offered and bids by the buyers on the ATS.

Alternative Trading System vs. Exchange

An ATS is similar to a traditional stock exchange in its functions - it constitutes buyers, sellers, and securities. But they differ in the way each functions. So now, let’s differentiate between an ATS and an exchange.

| Alternative Trading System | Stock Exchange |

|---|---|

| It should register under Exchange Act Rule 3a1-1(a). | It should be registered under Sections 12 (a) and 12 (b) of the Exchange Act. |

| Not self-regulatory; so it doesn’t have members, but subscribers | Self-regulatory; and has members. |

| Private operations. | Publicly disclosed operations. |

| Less regulated by the SEC. | Heavily regulated by the SEC. |

| Trades listed and unlisted stocks. | Trades listed stocks only. |

For professional-grade stock and crypto charts, we recommend TradingView – one of the most trusted platforms among traders.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

An individual or an entity can form an ATS by registering under Exchange Act Rule 3a1-1(a). It should comply with the requirements under Rules 300-303. The ATS should regularly file reports under Rule 301(b)(2).

According to the ATS list published by the SEC, there are 68 ATS legally recognized by the SEC. Every month this list is updated. In addition, information regarding the ATS that has ceased operations is published too.

There are mainly four types of ATS – dark pool, electronic communication networks, crossing networks, and call markets. Of these, the first two are the most prominent ones.

ATS matches buyers and sellers automatically. It allows investors to trade large securities with minimum to no regulations without having to disclose investment and investor information.