Table Of Contents

What Is An Adjustable Rate Mortgage (ARM)?

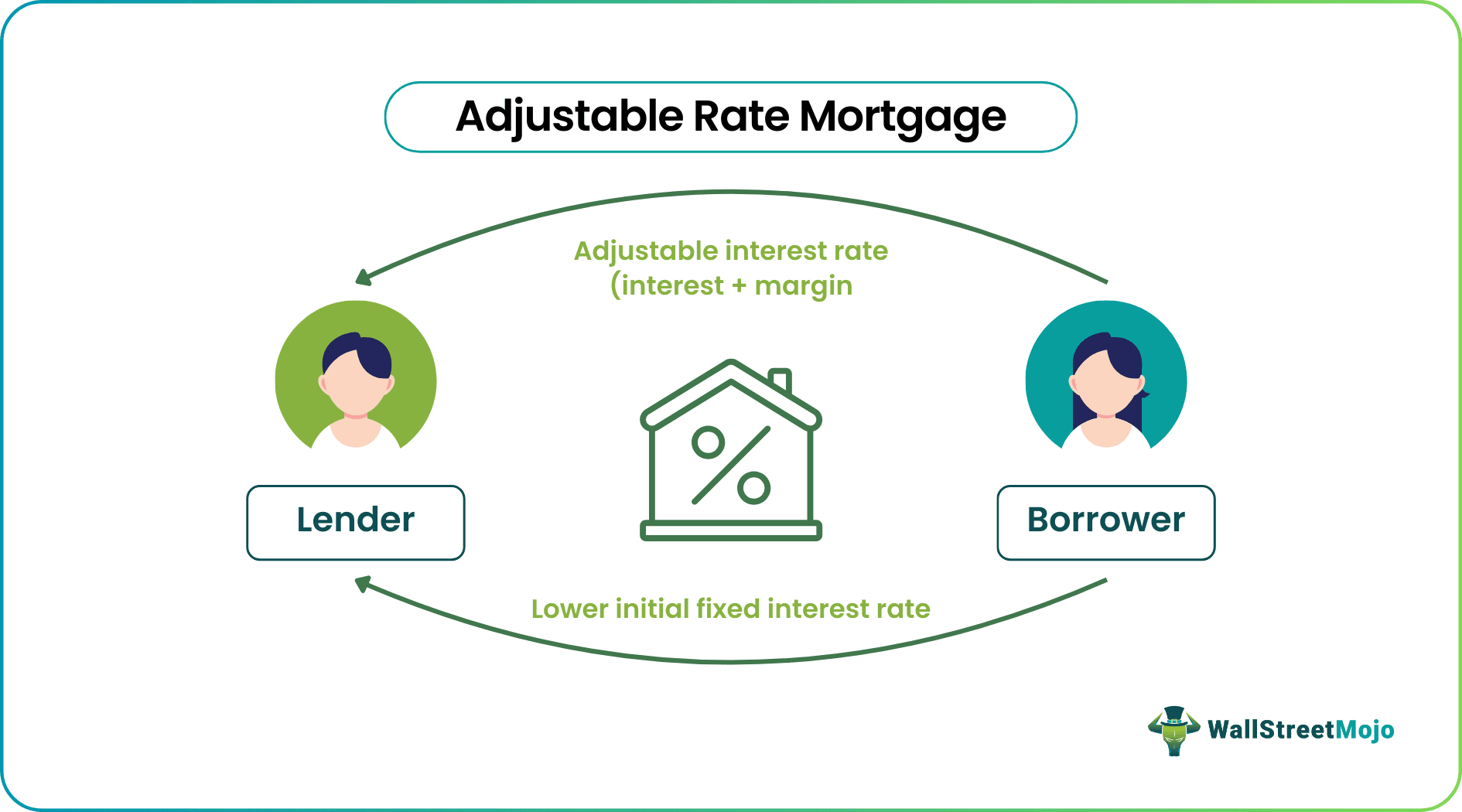

An adjustable rate mortgage (ARM) is a home loan where the interest rate is regularly adjusted and dependent on an index, such as the prime rate. It aims to determine the rate at which the borrower's monthly mortgage payment will change. As a result, its interest rate is generally lower than that of a fixed-rate mortgage.

It aims to make it a good option for borrowers who expect to sell their homes or refinance their mortgages before the interest rate adjusts. First, however, borrowers need to understand their loan terms and how the interest rate changes can impact their monthly payments. Though interest rates are lower, the monthly prices can fluctuate depending on the index changes.

Table of contents

- What Is An Adjustable Rate Mortgage (ARM)?

- Adjustable rate mortgages (ARM) have a lower initial interest rate than fixed-rate mortgages. However, the interest rate adjusts periodically, dependent on an index and a margin.

- The monthly loan payment can fluctuate dependent on changes to the index. As a result, it may be a good option for borrowers who expect to sell their homes or refinance their mortgage before the interest rate adjusts. This is why it is also known as adjustable-rate mortgage refinance.

- Borrowers should consider their financial situation and whether they can afford higher monthly payments if the interest rate increases.

How Does An Adjustable Rate Mortgage Work?

An adjustable-rate mortgage (ARM) loan is a home loan where the interest rate is adjusted periodically dependent on an index, such as the prime rate. The index determines the rate at which the borrower's monthly mortgage payment will change.

Here is an illustration of how it works:

- A borrower takes out a mortgage with a fixed interest rate for a certain period, usually 3, 5, 7, or 10 years. This initial period is called the 'introductory period' or 'teaser period.'

- After the introductory period, the interest rate will adjust periodically, typically yearly. The new rate is dependent on the margin and the index. The index, such as the prime rate, and the margin, are fixed amounts added to determine the interest rate.

- The borrower's monthly mortgage payment will also change when the interest rate adjusts. If the index goes up, the borrower's monthly income will increase. If the index goes down, the borrower's monthly payment will decrease.

- The terms of such loans will specify how often the interest rate can adjust and how much the interest rate can increase or decrease at each adjustment. This is called the 'rate cap.'

Borrowers need to understand the terms of such loans and how the interest rate changes can impact their monthly payments. In addition, borrowers should consider their financial situation and whether they can afford higher monthly fees if the interest rate increases.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types

Lenders can offer several types of adjustable mortgages. Here are a few examples:

- One-Year Adjustable-Rate Mortgage: This loan's interest rate adjusts yearly.

- Three-Year Adjustable-Rate Mortgage: The interest rate on this type of loan adjusts every three years.

- Five-Year Adjustable-Rate Mortgage: The interest rate on this type of loan adjusts every five years.

- Seven-Year Adjustable-Rate Mortgage: The interest rate on this type adjusts every seven years.

- Ten-Year Adjustable-Rate Mortgage: The interest rate on this type adjusts every ten years.

- Hybrid Adjustable-Rate Mortgage: This type of loan combines the features of a fixed-rate mortgage and an adjustable-rate mortgage. It may have a fixed interest rate for a certain number of years, and then the interest rate will adjust periodically. For example, a 5/1 adjustable-rate mortgage has a fixed rate for five years, and the interest rate adjusts yearly.

Example of ARM

Let us understand it better through the following examples.

Example #1

Suppose a borrower takes out a 5/1 adjustable mortgage with a fixed interest rate of 3.5% for the first five years. The index determines the interest rate as the prime rate, which is currently 3%, and the margin is 2.5%.

After the first five years, the interest rate will adjust every year, dependent on the index and the margin. Therefore, the new rate will be the sum of the index and the margin. In this case, the new rate will be 3% + 2.5% = 5.5%.

The borrower's monthly mortgage payment will depend on the new rate of 5.5%. So, for example, if the borrower had a loan of $200,000 with a 30-year term, the monthly payment would be about $1,136.

If the index goes up the following year, the borrower's interest rate and the monthly payment will also go up. For example, if the index increases to 4%, the new rate will be 4% + 2.5% = 6.5%, and the monthly payment will increase to about $1,220.

Example #2

The Federal Reserve continuously raised interest rates in 2022, which led to a sharp rise in adjustable-rate mortgage rates. Although a carefully watched mortgage rate trended downward, rates generally fluctuated over the previous week. Interest rates on fixed mortgage mortgages fell compared to increases in 15-year fixed mortgage rates. However, the mortgage with a 5/1 adjustable rate increased in variable rates.

Pros And Cons

Here are some pros and cons of adjustable-rate mortgages:

Pros

Some of its advantages are -

- Lower initial interest rate: Here, the interest rate is typically lower than that of a fixed-rate mortgage during the introductory period. This makes it easier for borrowers to qualify for a mortgage and may result in lower monthly payments.

- Potential for lower long-term interest costs: If the borrower expects to sell their home or refinance their mortgage before the interest rate adjusts, they may be able to take advantage of lower long-term interest costs.

Cons

The disadvantages of it are as discussed -

- Uncertainty: The monthly payments can change over time, making it difficult for borrowers to budget and plan for the future.

- Risk of higher payments: If the index used to determine the interest rate increases, the borrower's monthly payments will also increase. This makes it difficult for borrowers to afford their mortgage if they have a limited budget or a fixed income.

- Prepayment penalties: Some adjustable mortgages may have prepayment penalties, meaning the borrower will have to pay a fee if they sell their home or refinance their mortgage before a specific date.

Adjustable Rate Mortgage vs Fixed Rate Mortgage vs Variable Rate Mortgage

Adjustable-rate mortgages (ARMs), fixed-rate mortgages, and variable-rate mortgages are all types of home loans that can be used to finance the purchase of a home. Here are some key differences between these types of mortgages:

#1 - Adjustable-Rate Mortgage (ARM)

- The interest rate is periodically adjusted dependent on an index, such as the prime rate.

- The interest rate is generally lower than a fixed-rate mortgage, but the monthly payment can fluctuate dependent on changes to the index.

#2 - Fixed-Rate Mortgage

- The interest rate on a fixed-rate mortgage is fixed for the loan's full term.

- The monthly payment on a fixed-rate mortgage is the same as the loan's full term.

#3 - Variable Rate Mortgage

- The interest rate on a variable-rate mortgage can change over time.

- The monthly payment on a variable-rate mortgage can change dependent on changes to the index used to determine the interest rate.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Yes, it may be refinanced, and the process is the same as financing any other mortgage. However, this method results in the borrower replacing their current loan with a new, updated loan.

Some of the critical factors affecting it are:

- The Index

- The Margin

- The Rate Cap

- The Term of the loan

Yes, depending on the conditions of a specific loan and a benchmark rate index, payments may go up or down in response to fluctuations in interest rates. In some circumstances, going with an adjustable-rate mortgage rather than a fixed-rate mortgage might be a wise financial move that could result in thousands of dollars in savings.

Recommended Articles

This has been a guide to what is Adjustable Rate Mortgage (ARM). We explain its pros and cons, comparing it with fixed-rate mortgages, examples, and types. You can learn more about finance from the following articles –