Table Of Contents

Acquittance Meaning

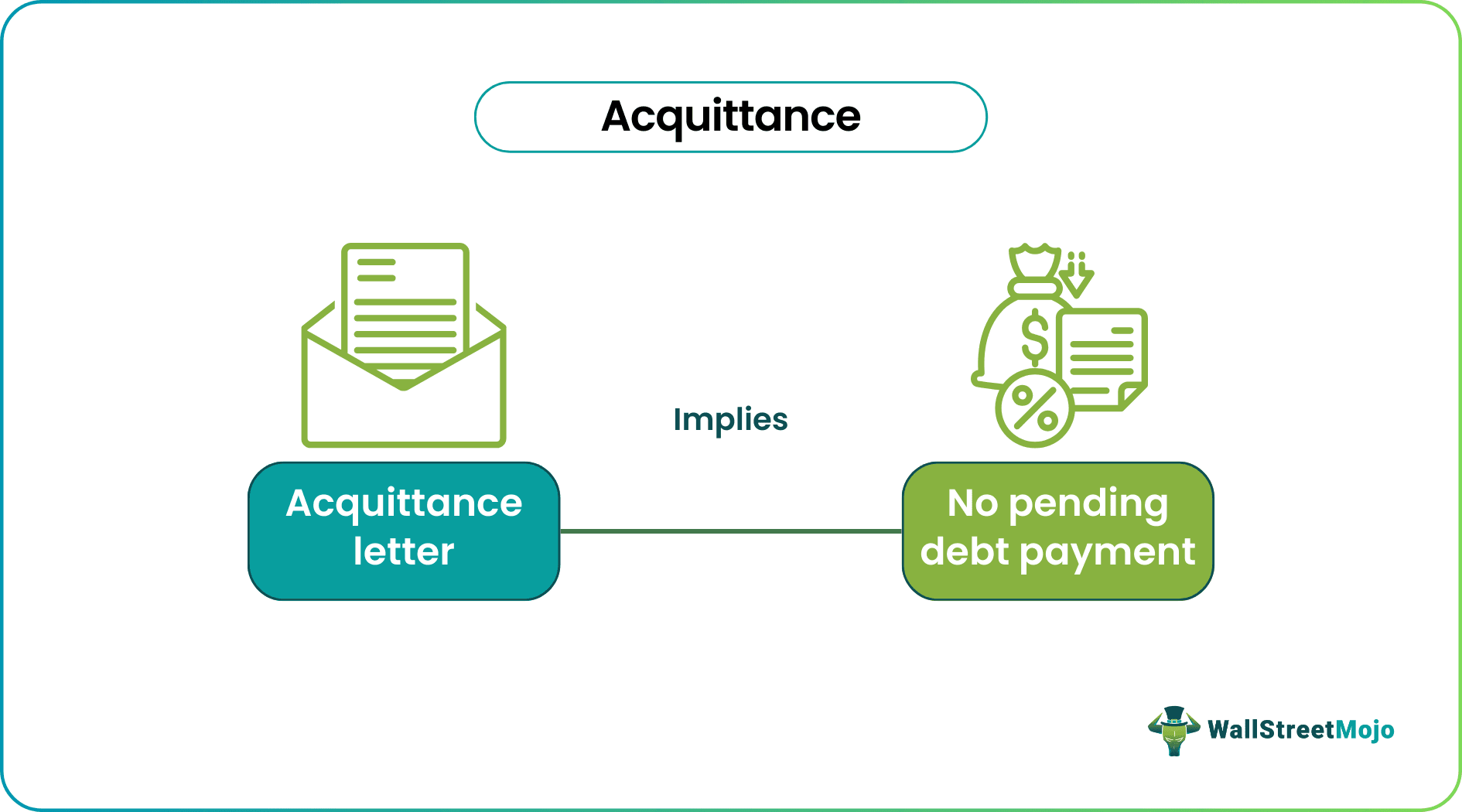

Acquittance is a legal document that declares the borrower has repaid the loan in full and is discharged from the debt. It is also known as the discharge letter. Every debtor must collect this document. Discharge letters are used to resell the property and apparent property disputes.

Lenders only send discharge letters to banks, financial institutions, and other creditors. Borrowers receive the document only after repaying the principal amount and the interests—when all the debt liabilities are cleared. An individual who defaults on their loan will never receive this document.

- The acquittance letter formally declares debt discharge. It is a crucial document that is used as proof of repayment.

- To receive the document, borrowers must clear pending liabilities like penalties and processing charges on top of the principal amount and interests.

- Borrowers receive discharge letters for both revolving loans and installment-based loans.

- When a person sells a property, the notary records all the loans and charges associated with the asset (cleared liabilities and outstanding liabilities). To prevent this, borrowers submit a deed of acquittance. It frees the property from the loan lender’s rights.

Acquittance Explained

Acquittance is a document that legalizes the completion of debt. It is written proof that the borrower has repaid the total loan amount with interest. This document frees borrowers from all liabilities associated with debt—repayment, penalties, fees, etc.

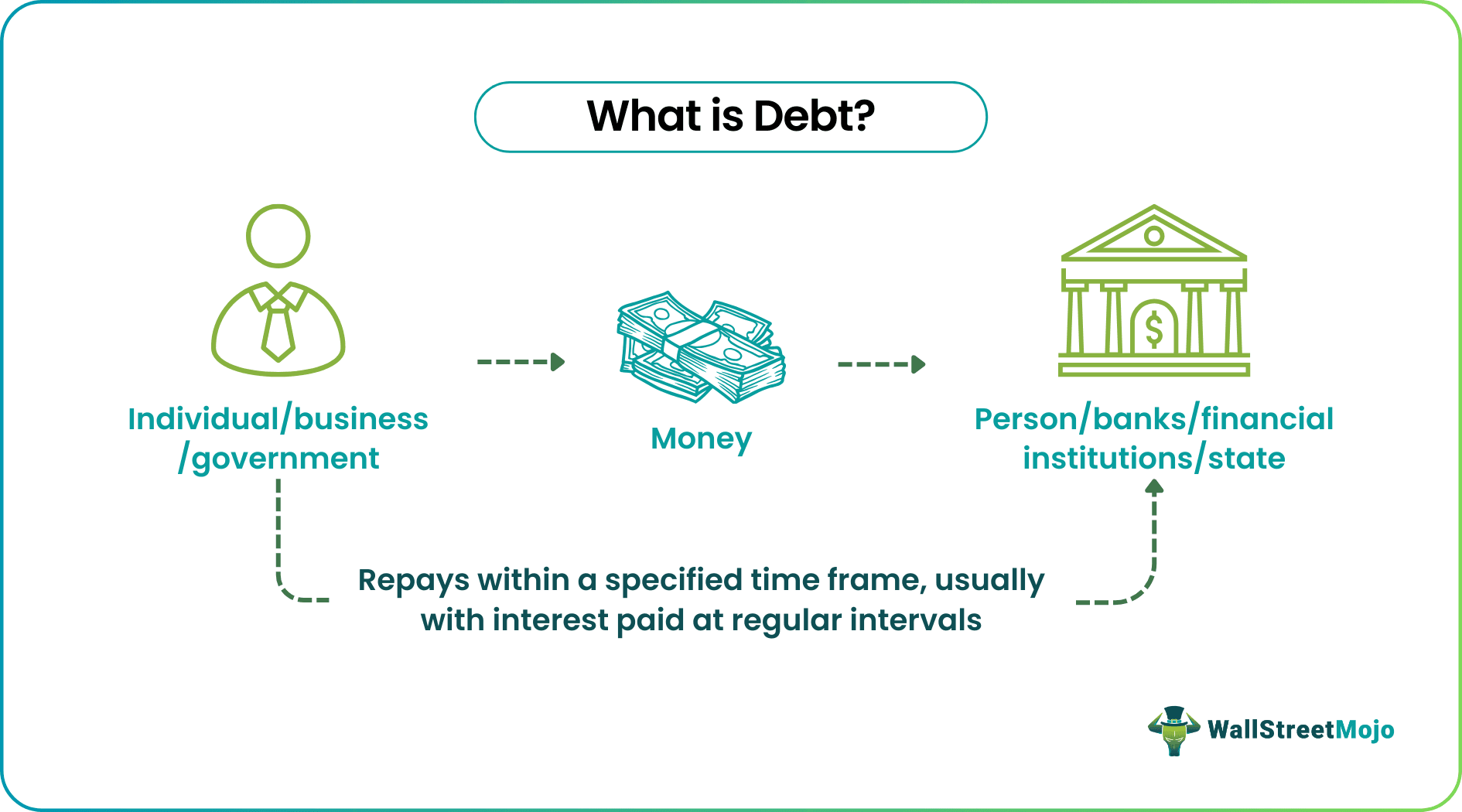

People apply for loans every day. Each loan comes with a specific interest and loan tenure. Most loans are sanctioned by commercial banks, mortgage lenders, financial institutions, or institutional lenders. Personal loans are further categorized based on the purpose of borrowing—car loan, home loan, education loan, etc.

In most cases, loan repayments are made via monthly installments. A part of regular repayments covers the principal amount; the remainder goes towards loan interests—lenders earn a profit through interest. Thus, when borrowers repay all those liabilities, they receive an acquittance letter from the bank or the lender.

It is also called a discharge letter. The letter mentions that the lender is satisfied with the borrower and has no pending liabilities. This procedure is standard for both monthly repayment loan structures and revolving loans.

A loan allows businesses to borrow varying amounts, depending on the business's cash flow needs. Here, the borrower pays a one-time commitment fee but is not restricted to a fixed-repayment schedule. Instead, revolving loans resemble credit cards—the business can repay in six installments (the principal plus the interest) or in one go.

Discharge letters are crucial. Borrowers are highly recommended to contact the bank or lender if they do not receive a discharge letter. There is a provision for requesting a discharge letter—borrowers must formally request it if they misplace it.

The most common usage of discharge letters is seen in property resales. If a property is used as collateral for a mortgage, future buyers will try to determine hidden liabilities, if any. This is where a discharge letter comes in handy. A discharge letter will assure prospective buyers that the property is debt free. Alternatively, discharge letters are beneficial in lawsuits—property disputes. It eliminates all kinds of confusion and miscommunication.

It is important to note that discharge letters are sent if a borrower repays in installments. However, a penalty is imposed if a borrower decides to repay early on. This is known as prepayment; it is a penalty imposed on a borrower for repaying too soon (before the completion of loan tenure).

Typically, lenders are not eager to close loan obligations too soon—they will lose earnings from interest. Therefore, prepayment is a hefty penalty, discouraging more borrowers from repaying too early. But, again, the borrower will receive the discharge letter only after paying the prepayment penalty.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Example

Let us look at an acquittance example to understand the document better.

Let us assume that Evelyn applies for a personal loan of $9000. She borrows the amount from a local bank. The bank explains to her that the loan carries an interest rate of 9% and a loan tenure of one and a half years. Thus, Evelyn will repay the loan in 18 monthly installments.

Evelyn will pay a monthly installment of $536.38, including interest. So altogether, Evelyn ends up paying $9654.82.

Evelyn works hard and repays her installments on time every month. At the end of the loan tenure (one and a half years), Evelyn pays the final installment, and the bank issues an acquittance document. This discharge later states that Evelyn has fully repaid her loan and is discharged from any bank obligations. The document mentions that the borrower has repaid the principal amount and the interest.

Discharge letters are essential documents; it is highly recommended that borrowers keep them safe. For example, if there is any confusion or data glitch, the bank might contact Evelyn saying repayment is pending. In such scenarios, producing the discharge letter clarifies the query.

Acquittance And Receipt Differences

Let us look at the difference between an acquittance and a receipt.

- Acquittance or a discharge letter is a debt discharge document; it declares that the borrower is free from the debt. In contrast, bank receipts are transaction documents.

- Discharge letters are sent only when the borrower completes the entire loan. On the other hand, bank receipts are provided for every payment (or transaction).

- Acquittances are provided only by a lender, whereas anyone can give a receipt. For example, a consumer may pay for a product purchased through a credit card and ask for a receipt.

- A discharge letter is an evidence that no further payment will be made to the financial institution; this is not the case with receipts.

- In recordkeeping, discharge letters are used to track loans and record credit history. On the other hand, auditors refer to receipts to ascertain the number of transactions made in a particular period.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

When a person sells a property, the notary records all the loans and charges associated with the asset (cleared liabilities and outstanding liabilities). To prevent this, borrowers submit the discharge letter—it frees the property from the loan lender’s rights.

A discharge letter is essential for the following reasons:

- Proof of debt discharge.

- Critical document for future reference.

- It is a mandatory procedure.

Although both are essential legal documents, invoices can be sent at any point of transaction, even when part of the payment is pending. In contrast, the discharge letter is sent only upon completion—when all the liabilities are cleared. An invoice is received by a person expecting payment; it contains all the transaction details. After that, a discharge letter is sent only by banks and lenders. It declares that the borrower is not liable for any further payments.

Recommended Articles

This article has been a guide to Acquittance and its meaning. Here, we explain it with an example and compare it with the receipt. You can learn more about it from the following articles -