What Is Accrued Payroll?

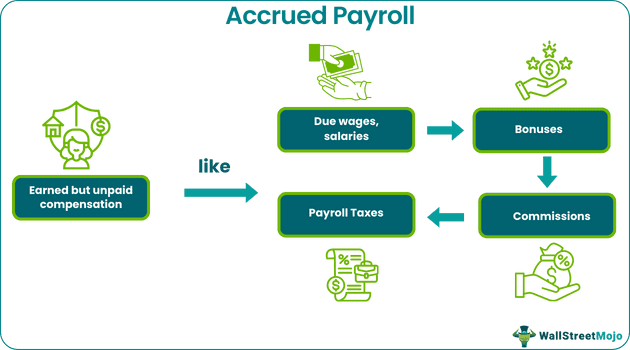

Accrued payroll is the earned but unpaid compensation of the employees that accumulates during a particular accounting period. Such accrued expenses include the due wages, bonuses, commissions, payroll taxes, and other costs. The purpose of this payroll is to help companies report their financial obligations and manage their cash flow accurately.

It is recorded as a liability in the company’s books at the end of an accounting period until the payment is made. In accrual accounting, the business records all those accrued expenses and incomes which are not paid or received in a specific accounting period. Therefore, accrued payroll is an important concept in accounting and financial reporting, reflecting the company’s obligation to its employees.

Key Takeaways

- The accrued payroll refers to the company’s current liability arising from accrued salary, wages, bonuses, commissions, payroll taxes, and other expenses.

- It is the total of all the earned but unpaid compensation of the employees during an accounting period.

- Thus, the company records the payroll accrual in its books (Balance Sheet) as a liability when it adopts the accrual method of accounting.

- Moreover, the company opens an accrued payroll tax account to record all the due but unpaid payroll taxes it is liable to pay to the IRS (Internal Revenue Service) on its employees’ behalf.

Accrued Payroll Explained

Accrued payroll refers to the amount employees have earned but have not received as a paycheck. Although the accrued payroll expense is due at the end of every pay period, the total of these unpaid expenses or payroll accrual is recorded in the books of accounts at the end of an accounting period. Hence, this accounting treatment is done when the company uses the accrual accounting method. This payroll method impacts a company’s cash flow, as it must pay its employees for work done even if the payment has yet to be made. Therefore, by recording the payroll accrual, a company can better manage its cash flow and ensure that it has adequate funds to meet its payroll obligations.

Furthermore, these payrolls are typically recorded by adjusting entries at the end of an accounting period, such as a month or quarter. Besides, the entry would increase the accrued payroll liability account and offset it with a corresponding expense account, for instance, the salaries and wages account. Moreover, the accrued payroll account is a liability account, which represents an obligation the company has to pay its employees.

Thus, it is a feasible method of accounting for irregular work hours or leaves in a pay period. Also, it helps in recording real-time expenses. Consequently, it lengthens the accounting process since keeping track of the employees’ work hours is tedious. To sum up, when an employer pays wages to its employees, it is responsible for withholding and paying the required accrued payroll taxes to government agencies. These taxes represent a liability on the company’s balance sheet until paid.

Journal Entry

The accrued payroll is treated as a liability in a company’s books of accounts. Thus, the general accounting rule applies here- debit all decrease in liabilities and credit all increase in liabilities. Accordingly, the payroll accrual is treated as follows in the journal entry books:

When the payroll expense is transferred to the accrued payroll A/c:

| Particulars | Debit | Credit |

|---|---|---|

| Payroll Expense A/c Dr To Accrued Payroll A/c | – | – |

The above journal entry reduces the payroll expense as the unpaid compensation is shifted to the accrued payroll account. It thus affects the income statement of the company. Also, the current liability, i.e., the payroll accrual, increases parallelly.

When the company pays off the accrued salary, wages, commission, bonus, or other payroll expense in the subsequent month:

| Particulars | Debit | Credit |

|---|---|---|

| Accrued Payroll A/c Dr To Cash A/c | – | – |

Or,

| Particulars | Debit | Credit |

|---|---|---|

| Accrued Payroll A/c Dr To Bank A/c | – | – |

Here, the business’s rapid asset decrease, and its current liability is also reduced.

Examples

Let us now discuss some practical examples of the payroll accrual below:

Example #1

Suppose a company’s sales executive receives a 10% commission on the sale of a product when the company realizes the payment from the buyer. The sales and accrued commission of the executive for three months from his joining are as follows:

| Month | Sales | Commission Earned | Commission Received | Accrued Commission |

|---|---|---|---|---|

| January | $19100 | $1910 | – | $1910 |

| February | $27700 | $2770 | – | $4680 |

| March | $51500 | $5150 | $1910 | $7920 |

| Total | $98300 | $9830 | $1910 | $7920 |

Also, he was promised a bonus of $2000 on attaining a quarterly sales target of $75000. Thus, the total accrued payroll is as follows:

Accrued Payroll = Accrued Commission + Accrued Bonus = $7920 + $2000 = $9920

Example #2

Suppose a company pays its contract labor hourly and disburses its wages at the end of the day. On the day of closing, i.e., on December 31, 2022, the laborers were paid based on their average working hours since they were not known at the close. However, the laborers worked for two extra hours that day, and their unearned wages amounted to $150. Thus, it is considered the accrued expense and recorded in the books as a liability. Although, the accrued wages were paid on the next day. The journal entries passed in this context are as follows:

Transferring the due wages to the accrued wages account:

| Particulars | Debit | Credit |

|---|---|---|

| Wages A/c Dr To Accrued Wages A/c | $150 | $150 |

Paying off the accrued wages:

| Particulars | Debit | Credit |

|---|---|---|

| Accrued Wages A/c Dr To Cash A/c | $150 | $150 |

Taxation

These payrolls are also subject to taxation like any other form of payroll. In addition to the taxes withheld from employees’ paychecks, employers are also responsible for paying their portion of payroll taxes. Therefore, when employers pay taxes to the Internal Revenue Service (IRS) on behalf of their employees, the same is to be deducted from the employees’ due compensation. It is, thus, termed payroll tax. The companies usually prefer paying the payroll taxes to the IRS at the end of each quarter. Hence, the firm maintains an accrued payroll tax account for recording such accrued tax liability.

The employer makes the following payroll tax deductions from the employee’s income:

- Federal income tax

- Social Security tax

- Medicare tax

- One-half of the Federal Insurance Contributions Act (FICA) taxes

- Other state and local taxes

The employees’ 401(k) contribution is deducted from their pretax payroll.

Frequently Asked Questions (FAQs)

1. How to audit accrued payroll?

Auditing this payroll involves thoroughly reviewing a company’s payroll records and related financial statements to ensure that the amounts recorded accurately reflect the company’s payroll obligations. There are a few steps that an auditor might take when auditing them, including:

· Understanding the company’s payroll policies

· Test the accuracy of payroll calculations

· Verify the accuracy of payroll-related accounts

· Reviewing the company’s internal controls

· Analyze the company’s payroll trends

2. Is accrued payroll an asset?

No, accrued payroll is not an asset. Instead, it is a liability on a company’s balance sheet as it is a debt owed by the company to its employees and is recorded as a liability until the payroll is paid out.

3. How to calculate accrued payroll?

Following are the steps for payroll accrual calculation:

– Determining the pay period

– Evaluating the number of hours worked by each employee

– Considering the employee’s hourly rate

– Multiply the hours worked by the hourly rate

– Add up the total earnings for all the employees

– Record the payroll accrual

Recommended Articles

This article has been a guide to what is Accrued Payroll. We explain the topic in detail, including its journal entry, examples, and taxation. You may also find some useful articles here –