Table Of Contents

What Are Accrued Expenses?

Accrued Expenses are expenses incurred and for which the payment has not yet been made. As a result, liability for these expenditures is created and recorded as accrued liabilities (short term) on the balance sheet liability side. When a business pays cash to settle such a responsibility, the expense account will be debited, and the accrued expense account will be credited.

The journal entry for accrued expenses is made as a current liability, which signifies that the amount due should be paid within a 12-month period to be reflected on the final balance sheet figure.

Table of contents

How Do Accrued Expenses Work?

The meaning of accrued expenses signifies expenses incurred but not paid by the business during the accounting period. These expenses are reflected on the business's balance sheet under short-term liabilities and should be monitored closely by those tracking the business. Its performance and changes in such expenses should be duly accounted for in the profit reported by the business.

The Principal of Accrual Accounting requires that expenses be recorded as the firm incurs them irrespective of whether actual cash has been paid. Therefore, it helps in the proper measure of the performance of a business during a reporting period as it accounts for the expenses incurred (although not due to be paid) with the associated revenues of the reporting period. Also, it helps avoid misstatement of the financial performance of the business. It enables various stakeholders to analyze the business to perform better and gain investors' confidence as GAAP compliant.

A most popular example of accrued expense includes Salaries payable as companies typically pay their employees at a later date for work done in the prior month.

The changes in Accrued Expenses should be closely monitored by those analyzing the business's financials. An increasing trend in such expenses signifies that the business is not honoring the expenses. As such, the profit reported is overstated as there will be an increase in cash flow and such increase in Accrued expenses to the extent to which they relate to the period must be adjusted from reported Profits to get a clear picture of the profit earned by the business in the period to which such expenses are associated.

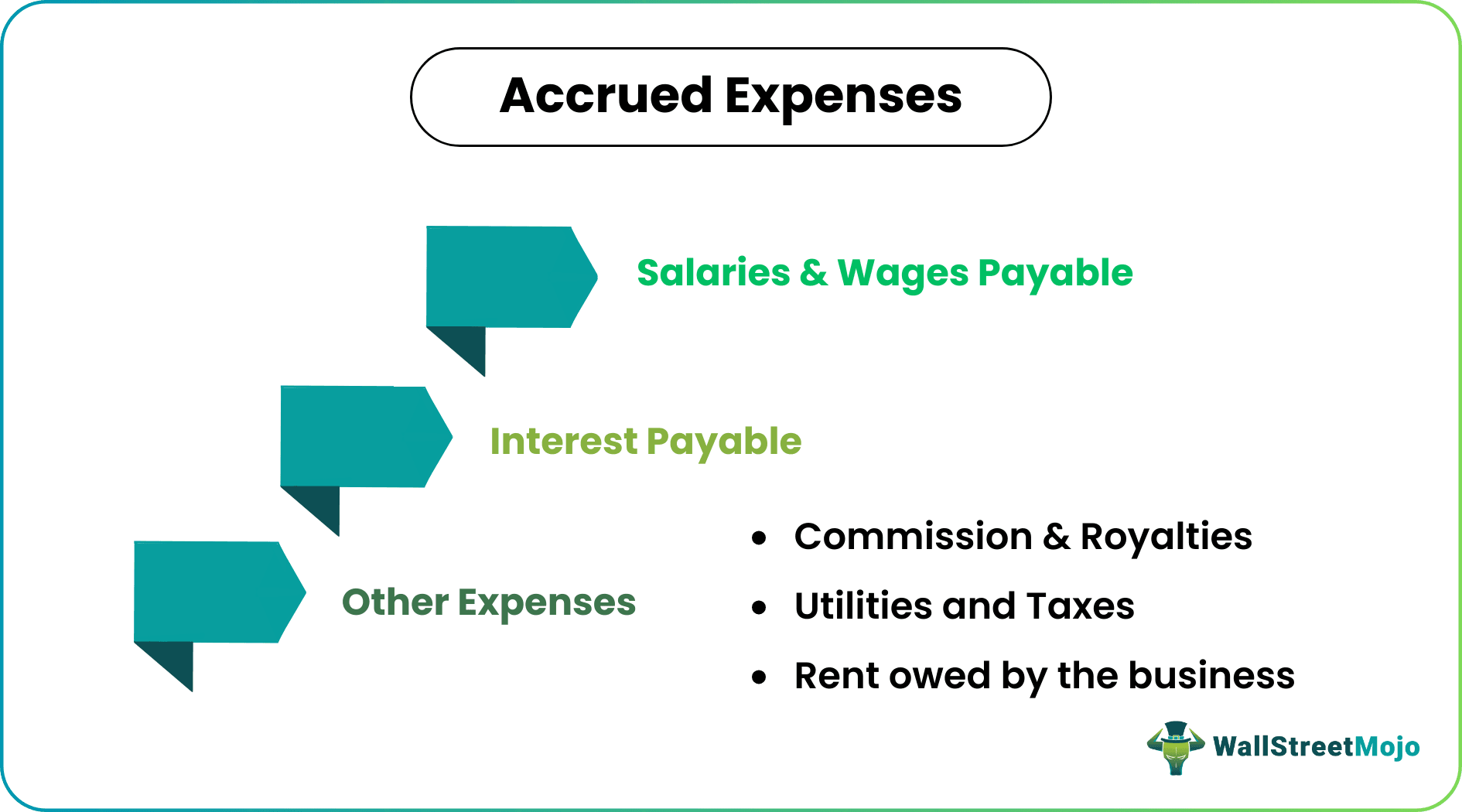

Types

#1 - Salaries and Wages Payable

These are the income due to the employees for the work done and are usually paid weekly or monthly. For instance, the work done by employees of Alex International is paid in the next month. Accordingly, it should be recorded by debiting Wages and Salaries Expenses, crediting Accrued Expenses, and making an offsetting entry by debiting these expenses and crediting cash when payment is made.

#2 - Interest Payable

It refers to the interest expenses which have occurred but are not yet due to being paid by the business. An adjusting entry needs to be passed on recording the impact of such an accrued interest.

Let's understand the same with the help of an example:

XYZ Company borrowed $100,000 on October 1, 2018, and requires making the complete repayment on January 31, 2019, along with interest of $5000. Therefore, as of December 31, 2018, it is not necessary for XYZ to make any interest expenses. However, $3750 ($5000*3/4) of Accrual expenses has occurred and will consist of debt of $3750 of interest expense and a credit of $3750 to the Interest Payable Account.

#3 - Other Expenses

Other examples may include the following

- Rent owed by the business but not yet paid.

- Commission and Royalties are yet to be paid by the business.

- Utilities and Taxes owed but not yet paid by the business.

How To Record?

Let us take an example of Starbucks to see the accrued expenses on the balance sheet:

source: Starbucks SEC Filings

The list of accrued expenses in Starbucks is –

- Accrued Compensation and Related Costs

- Accrued Occupancy Costs

- Accrued Taxes

- Accrued Dividends Payable

- Accrued Capital and other Operating Expenditures

Examples

Let us consider the following examples of accrued expenses to understand the concept well:

Example #1

Gluon Corporation operates in the Pharmaceutical Industry and pays a fixed 2% commission on Monthly Turnover payable on the 7th day of the next month. The Company achieved a turnover of $40000 during the month ending December 31, 2018. However, the commission was payable on January 7, 2019, and as such, the following journal entries will be passed to record the Accrual commission of $800 ($40000*2%)

Example #2

Matija Square has a five-day working week, and payday is Friday of each week. Therefore, weekly salaries are $5000. The current Accounting period ended on Thursday, December 31, 2015. Therefore, Matija Square will adjusting journal entries to account for the Wages accrued of $4000 ($5000*(4/5)).

Example #3

Flour International utilized the services of an Electrician to repair the light fixtures in their retail shop on December 24, 2018, which resulted in an expense amounting to $300.The electrician sent the bill to Flour International on January 3, 2019. As a result, flour International will report the $300 expenses as Accrued Expenses on its Balance Sheet and will reduce the associated amount of $300 from its Income Statement on December 31, 2018; however, the actual payment will be made on January 3, 2019.

Recommended Articles

This article has been a guide to what are Accrued Expenses. Here we explain it with examples with steps of how to record them, their types, and how they work. You can learn more about accounting from the following articles –