Table Of Contents

What Is Accounts Payable (AP) Cycle?

Accounts Payable cycle, also known as 'Procure to Pay' or 'P2P cycle, is a series of processes involving the company's purchase and payments department and carrying out all necessary activities from placing an order to suppliers purchasing goods and making final payments to the suppliers.

Thus, it is the cycle or the process that the business follows when they buy goods and services from other vendor companies and make payment for them. This cycle helps the purchaser keep track of the payments to be made, whether they are being made on time, and the amount of cash outflow taking place during a particular period.

Table of contents

- he accounts payable cycle is a set of procedures that involves the company's purchasing and payments division in carrying out all essential tasks, from placing an order to having suppliers buy items to paying the suppliers in full.

- Purchases, supplier payments, manufacturing costs, salaries, and wages, among other expenses, are all part of the expenditure cycle. The spending cycle includes the accounts payable process in considerable measure.

- The documents required in the accounts payable cycle are the purchase order, receiving the report, and the vendor invoice.

Accounts Payable Cycle Explained

The accounts payable cycle is followed by the business paying vendors who have supplied goods and services to them. This cycle is a method that ensures that the required products are correctly ordered and the purchase order is sent to the supplier on time so that the stock is replenished and available for use in the business.

A full accounts payable cycle then keeps track of the invoices received for payment, the details are properly checked and tallied with the order to confirm the price, quantity, tax, freight, type of product, etc, which are entered in the system for initiating the payment process. However, the purchasing department should check whether the goods are received or not.

The cycle also involves verification and account reconciliation to settle any kind of discrepancy and dispute so that the books remain transparent and clear. The business is able to track whether payments are made on time and in the correct amount.

Every business has two major Business cycles - revenue cycle and expenditure cycle.

- The Revenue Cycle includes sales, marketing, customer relationship, revenue collection, etc.

- The Expenditure Cycle includes purchases, supplier payments, production expenses, wages, salaries, etc. The accounts payable cycle is a significant part of the expenditure cycle.

Accounts Payable Explained in Video

Steps

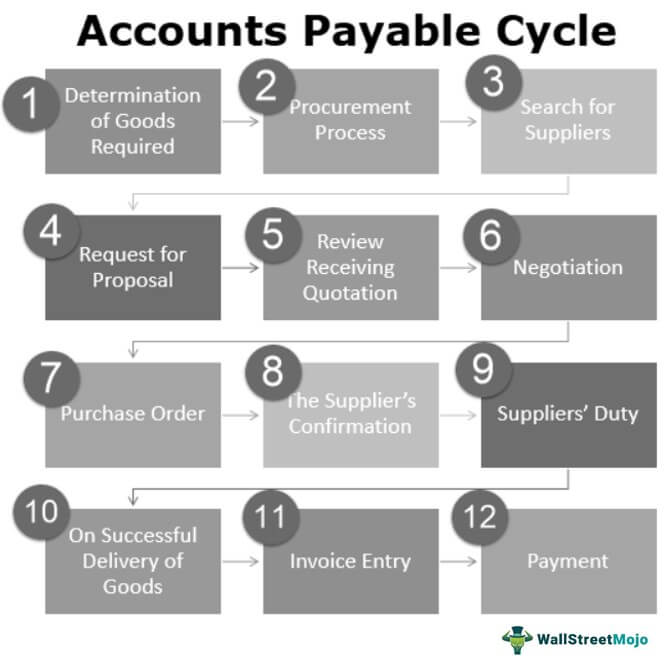

Following are the steps included in the Accounts Payable Cycle –

- Determination of Goods Required

- Procurement Process

- Search for Suppliers

- Request for Proposal

- Review Receiving Quotation

- Negotiation

- Purchase Order

- The Supplier’s Confirmation

- Suppliers’ Duty

- On Successful Delivery of Goods

- Invoice Entry

- Payment

Therefore the above are the accounts payable cycle steps that companies usually follow.

Flowchart

Let us discuss these in detail -

A full accounts payable cycle is the series of different processes in the company involving the different activities required for the purchase of the product right from placing the order for the goods to the suppliers, then purchasing and getting delivery of the goods and finally making the final due payment to the supplier against the same.

The following are the accounts payable cycle steps or procure-to-pay cycle steps.

#1 - Determination of Goods Required

The purchases are made based on the stocks required by the company's Production Department. The production manager identifies the needed supplies and informs the purchasing department.

#2 - Purchase Department starts the Procurement Process

After getting the approval of supplies requests from production, the purchasing department will look if some similar orders have already been placed; if not, new documents of purchase orders are generated.

#3 - Search for Suppliers

Finding suppliers is a tricky job that includes various factors like locality, ease of transport, credit policies, goodwill of supplier and its products, past connections with the company, and many more. However, the company prefers transactions with its tried and tested suppliers. In other cases, potential suppliers are selected locally, nationally, or internationally using an online business-to-business portal (like Alibaba.com), referrals, etc.

#4- Request for Proposal

After selecting a few potential suppliers, a formal document is delivered to receive quotations of the items. The supplier sends a proposal, including product rates and qualities, and asks the company to do business with them. The document is referred to as a request for proposal (RFP).

#5 - Review Receiving Quotation

The company reviews the quotations from different suppliers and filters the suppliers who can fulfill the company's requirements. The company informs the selected suppliers about its interest in making purchase deals.

#6 - The company begins the Negotiation Process

Negotiation is a hectic and sometimes time-consuming process. The buyer requests the seller to lower its rates, offer a liberal credit policy, and other basic negotiation terms like discounts, quality of products, freight charges, delivery, and insurance terms. The negotiation process performs the filtering, and the company has identified the best suppliers.

#7 - Purchase Order

On approving the desired supplier, the company awards him the order by sending the official purchase order document. It confirms the supplier about the company's requirements and the deadline for delivering the products or services.

#8 - The Supplier’s Confirmation

The agreement initiates when a supplier agrees to sell its products at the requested terms and conditions. The supplier must send a confirmation of acceptance in writing through post or email.

# 9 - Suppliers’ Duty

The supplier must get the goods ready and shipped following the deadlines strictly and keep the company informed about the order progress. Notification must be sent when goods are ready to be shipped and a shipment notice, including valid documents specifying a description of goods, weight or units, delivery date, location, etc.

#10 - Inspection of Delivered Goods

The process of inspection begins, which includes both quality and quantity checks. The purchase department checks if delivered goods are according to the purchase order.

#11 - Invoice Entry

On successful inspection, if everything finds fit, the purchasing department sends the approval to the accounts payable department to begin the payments process. The accounts payable department thus makes a record of the invoice, which contains all the specifications about the payment like the final date and a final date with discount, amount of reimbursement, and other official details.

#12 - Payment

After every necessary check, the accounts payable department starts payments to the supplier partially or fully as per company norms. There are various ways to make payments to the suppliers like:

- Cash payments

- Cheque payment (or other negotiable instruments)

- Online third-party transfer

- Credit Card Payment

- Payments in dollars or other foreign currency (generally applicable in import transactions);

- Barter payment, i.e., paying some goods and/or services against the goods and/or services received by the supplier.

Example

Let us assume that Skyline Ltd is a sports goods manufacturing company which purchases its raw materials from Sportsline Ltd. Thus, Skyline Ltd has to regularly maintain the accounts payable cycle to keep track of the inventory coming in, the credit terms, the payment amount and date, etc.

The company has a good name in the market due to its transparent way of dealing with customers, making payment on time and supplying quality products in the market. Any discrepancies with clients are immediately settled and for that reason it gets good credit terms, helping it to maintain a healthy cash flow.

Relevant Documents

The following are important documents included in procure to pay cycle:

#1 - Purchase Order

The company's purchasing department generates an order of the required goods and sends it to the vendor. The order details the vendor about the items along with their quantities. It also specifies a date on which the goods must be delivered.

#2 - Receiving Report

After the goods are delivered, the management inspects the shipment and checks the quality, quantity, and other essential aspects. After a full inspection, it creates a detailed report called receiving the report.

#3 - Vendor Invoice

The document is the legal contract in which the vendor details the goods, the rate per unit, the total amount, and the appropriate taxable amount. It also specifies the credit policy and the final date for payment.

Advantages

The cycle has some advantages as given below:

- Better cash management – If the method is implemented properly, then the business can manage its cash flow effectively an at the same time maintain good customer relation and get good payment terms.

- Good financial reporting – The cycle involves clear recording of financial transactions regarding payment and keeping track of the entire order in details. This ensures transparent financial reporting.

- Good customer relation – If payment is made on time, the suppliers become more interested in doing business with such companies and may provide extra credit period or charge less prices.

- Bugeting – It is possible to understand the expenses that is being incurred or will be incurred for this kind of purchases and accordingly plan for future by keeping aside funds for similar purchases, Thus ensures there is no fund wastage and good financial management.

Disadvantages

Along with advantages, the cycle has some disadvantages also:

- Penalty for late payment – If the business is not able to manage the cycle properly, they will have to pay penalty for delayed payment.

- Problems with cash flow – The process may lead to cash crunch if payments are made before time. If paid before time, then the entity should also ensure that its receivables are collected on time.

- Risk of fraud – There is always a risk of committing fraud by entering improper figures, impersonating the vendor representative to collect payment, etc.

- Vendor–purchaser relation risk – If the cycle is not strictly followed, it may result in damaging the relation of the buyer with the seller.

Thus, overall, the process is very useful for any business if followed properly and helps in maintaining good financial health of the company.

Frequently Asked Questions (FAQs)

The accounts payable cycle focuses on a company's obligations to pay its suppliers for goods or services received. On the other hand, the accounts receivable cycle revolves around the company's efforts to collect customer payments for goods or services. Both cycles are critical components of a company's cash flow management.

The stages in the accounts payable cycle are: receiving the invoice, reviewing the invoice, approving the invoice, and finally paying for the invoice.

The entire cycle of the accounts payable process includes the following:

The collection of invoice data.

The coding of invoices with the proper account and cost center.

Authorizing invoices.

Connecting invoices to purchase orders.

Posting for payments.

Recommended Articles

This article has been a guide to what is Accounts Payable Cycle. We explain its flowchart along with steps, example, relevant documents, advantages & disadvantages. You may learn more about financing from the following articles –