Accounting vs. Auditing

Accounting is an act of maintaining the monetary records of a company to help prepare financial statements, which will give an accurate and fair view of the company’s business. As we note from Colgate’s SEC Filings, they must prepare the financial statements as per the regulatory authority guidelines.

On the other hand, auditing evaluates financial records/statements prepared through the accounting function. The purpose is to ensure the reliability of the financial statements. For example, in the case of Colgate, PricewaterhouseCoopers LLP audited the effectiveness of Colgate’s internal control over financial reporting in 2016.

In this article on Accounting vs. Auditing in greater detail –

What is Accounting?

Accounting is the language of business. Any business is measured in terms of numbers, and these numbers are arrived at by employing accounting. Let us take simple examples of what kind of numbers are required by any businessmen on a day to day basis:

Key Takeaways

- What is the quantity of goods sold in the current month/quarter/year?

- What is the total cost incurred during the month/quarter/year?

- Is the company earning a profit or incurring heavy losses? In either case, what is the quantum of this profit/loss? What is the proportion of profit/loss as compared to the total sales?

- How much is the saving (positive saving will represent a benefit whereas a negative saving will denote that the company has spent more) in the cost compared to last month?

- How many employees are currently employed in the organization?

- What is the profit margin the company?

- What is the growth of the company over the past ten years?

- What is the total market share of the company?

- What is the profit of each retail outlet for the company?

Accounting vs Auditing – Explained in Video

The above questions can be answered utilizing accounting. Accounting has various branches, such as:

#1 – Financial Accounting

The main focus of financial accounting is maintaining, processing, grouping, summarizing, and analyzing the company’s financial information to give an accurate and fair view to various internal and external stakeholders of the company.

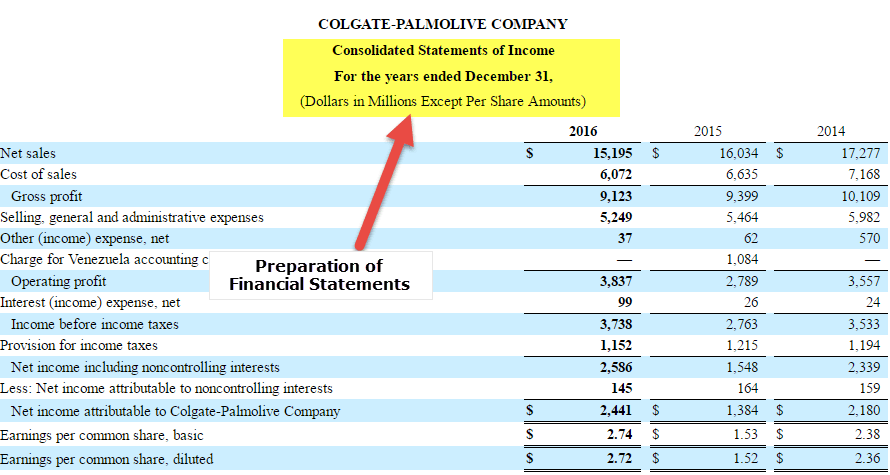

As we see from the below snapshot taken from Colgate 10K, the main focus of financial accounting is to prepare the financial statements, namely the Income Statement, Balance Sheet, and Cash Flow.

source: Colgate 10K Filings

Following is the graphical representation of the financial accounting process:

#2 – Cost Accounting

Cost accounting is beneficial from the point of view of costing various products. It helps to derive a cost price for complex products that require various raw materials, processes, and ingredients in their manufacture. It also helps to identify the key costs (fixed and variable) associated with each product and the break-even point for the products.

This serves an essential purpose for any given company. First, it derives a cost, which helps to calculate the selling price of the product. The selling price will be derived based on various parameters such as the company’s margin percentage, market competitiveness, the strategy involved in selling the product, etc.

If you want to learn Cost Accounting professionally, you may want to look at 14+ video hours of Courses on Cost Accounting.

#3 – Managerial Accounting

This section has more to do with planning and support decisions. The data organized by other fields of accounting are analyzed further to plan, make strategic decisions, and prepare a roadmap. Here, reports (MIS – Management Information System) are prepared daily/weekly/monthly for internal audiences such as the chief financial officer, chief executive officer, managers, and other top-level executives who make informed decisions on behalf of the company. The reports help them get a better perspective and make informed decisions. Some of these decisions involve – capital budgeting, trend analysis, forecasting, etc.

Some other types of accounting are Tax Accounting, Human Resource Accounting, Government Accounting, etc.

What is auditing?

Auditing is an activity of verifying, checking, and evaluating financial statements. As the financial statements are prepared based on an organization’s accounting records, auditing covers the checking of accounting records.

It helps determine the validity and reliability of accounting information represented using financial statements.

Auditing can be said to be more of a post-mortem activity. Once the financial accounting process is completed for a given year, the auditing process can start.

Auditing can be divided into External audits and Internal Audit

| costing various products |

:

| costing various products |

Accounting vs. Auditing – Top 11 Differences

| Sr. No. | Point of Difference | Accounting | Auditing |

| 1 | Definition (Accounting vs. Auditing) | Accounting is an act of maintaining the monetary records of a company in a way that they can help in the preparation of financial statements, which will give an accurate and fair view of the business of the company. | Auditing is the evaluation of financial records/statements prepared through the accounting function. The purpose is to ensure the reliability of the financial statements. |

| 2 | Regulators (Accounting vs. Auditing) | Accounting Standards are issued by International Accounting Boards, which need to be adhered to while preparing financial statements. | Auditing Standards are issued by International Auditing Boards, which need to be adhered to while auditing financial statements. |

| 3 | Aim (Accounting vs. Auditing) | To provide an accurate and fair view of the financial statements to various users | To verify the reliability of the financial statement’s true and honest view |

| 4 | Main Categories (Accounting vs. Auditing) | A few sub-heads of accounting are as follows:

| Auditing can be bifurcated into:

|

| 5 | Key Deliverables (Accounting vs. Auditing) | Financial Statements is the critical deliverable of accounting, and the same comprises of the following:

| An audit report is a vital deliverable of auditing, and the same can be classified into the following:

|

| 6 | Work is performed by (Accounting vs. Auditing) | Bookkeepers and accountants | Auditors (It is essential for an auditor to have knowledge of accounting. Without thorough knowledge, an auditor cannot certify the financial statements. On the other hand, an accountant need not be well-versed with the auditing processes) |

| 7 | Key skills required (Accounting vs. Auditing) | Some of the critical skills needed by an auditor are:

| Some of the critical skills required by an auditor are:

|

| 8 | Day-to-day activities involved (Accounting vs. Auditing) | Daily operations of an accountant will include the following:

| Day-to-day activities of an auditor will involve the following:

|

| 9 | Level of responsibilities (Accounting vs. Auditing) | An accountant is part of the middle-level management of the organization. Here, the responsibility is to present a true and fair view of the financial position of the company to various stakeholders. Note: A thorough background check is required in this case as the accountant is in a position to manipulate the financial results of the company. | An auditor can be internal as well as external to the organization. In the case of an internal auditor, he/she will be part of the middle-level management of the organization. In the case of an external auditor, companies opt for certified auditing firms that are well-known in the industry. In a way, the level of responsibility of the auditor is more than the accountant. The report issued by them is a certification of the work done by the accountant. Note: A thorough background check is required, even in this case, because an auditor certifies the work of an accountant. If an auditor is not careful in performing his / her duties, there can be ample fraud opportunities to the accounting team. |

| 10 | Starting point (Accounting vs. Auditing) | The starting point of accounting is Bookkeeping, i.e., maintaining records of the financial affairs of the company, which is then used to prepare the financial statements of the organization. | Auditing starts when the work of an accountant is complete. Once the financial statements are prepared, the auditor starts verifying the completeness and accuracy of the financial statements. |

| 11 | Period (Accounting vs. Auditing) | It is an on-going activity. The financial statements can be prepared on a quarterly and annual basis, but recording journal entries and other accounting functions are a continuous process. | This is a periodic activity. An annual audit of the financial statements is a statutory requirement in most countries. Many companies prefer to conduct an audit on a quarterly basis as well. |

Conclusion

Accounting vs. auditing are interrelated and go hand in hand with each other. The job done by the accountant is certified by the auditor. The auditor’s job will have no meaning if the basic accounting framework is not established in the organization. Also, if there is no one to certify the work done by the accountant, there will be surety about the reliability of the data presented in the Financial Statements. An auditor adds value to the work done by the accountants.

Also, the two can work hand-in-hand, especially in setting up processes in the organization. The auditor can test the controls designed and implemented by the accountant. Control gaps, if any, which are high-risk areas, can also be pointed out by the auditors. The auditors can use their experience and expertise and provide feasible suggestions/solutions for process improvements. The accountant, for better risk management, can implement these.

These internal controls, which are set by the accountants and auditors together, are generally approved by the management. They can be as simple as a manual maker-checker system where a maker will prepare a document (e.g., a cash voucher) and get it approved by a superior. These controls can also be as complex as an inbuilt feature in the ERP, highlighting and disallowing the creation of a duplicate vendor ledger by checking the unique company identification number.