Table of Contents

What Is An Account Titles In Accounting?

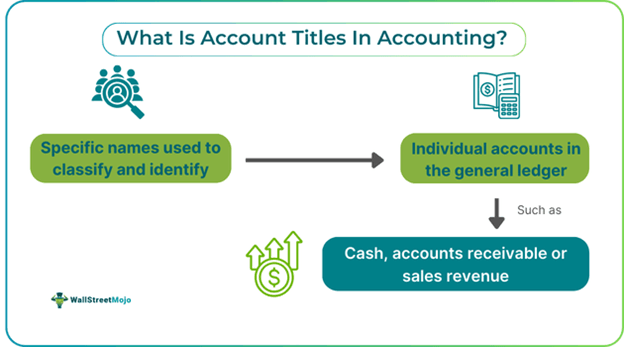

Account titles are names of categories in accounting that track a business's finances. They are updated for each transaction to ensure an organized and consistent record. These titles are part of the business's general ledger, which is a running list of all transactions.

Each title serves a unique purpose in effectively recording and reporting financial data. They are critical for organizing financial information and accurately recording, analyzing, and reporting on a company's financial activity. They provide a uniform structure for documenting transactions, making it easier to compare, make decisions, and comply with accounting rules and requirements.

Key Takeaways

- Account titles are specific names assigned to accounts in a company's general ledger, used to record, categorize, and summarize transactions.

- They play a crucial role in financial management, compliance with accounting standards, strategic planning, internal control, fraud prevention, and building investor confidence.

- These titles are categorized into assets, equity, revenue, and expenses, each serving a distinct purpose.

- Assets and equity reflect immediate or projected economic benefits, while revenue accounts track income generation.

- Expense accounts handle financial transactions related to costs, ensuring regulatory compliance, transparency, and the protection of shareholder interests.

Account Titles In Accounting Explained.

Account titles in accounting are the names assigned to specific accounts in a company's general ledger. The ledger represents a company's assets, liabilities, equity, revenue, and expenses. Account titles assist in determining the type and purpose of an account and recording, categorizing, and summarizing transactions in the company's financial records. These titles are essential for categorizing financial data and creating financial statements such as balance sheets and typical income statements.

Account titles and explanations should be descriptive, clear, and adhere to accounting principles and standards. They are usually decided by the chart of accounts, which is a list of accounts used in a company's financial reporting system. Account titles are essential in accounting for a company's financial management, providing a standardized framework for recording and organizing financial transactions. They enable accurate financial reporting, compliance with accounting standards, strategic planning, internal control, fraud prevention, and investor confidence.

Account titles and explanations help in understanding and also facilitate comparison and analysis of financial information across different companies and industries, aiding investment analysis and decision-making. Account titles also facilitate effective communication with stakeholders, including shareholders, by providing a common language for discussing financial matters. They are crucial for meeting regulatory requirements and maintaining transparency in financial reporting, protecting the interests of shareholders and the general public. Overall, account titles are essential for a company's financial health, compliance, and investor protection.

Types

The type of account titles are given as follows:

#1 - Asset category

The account titles under assets refer to accounting transactions that attempt to provide immediate or projected economic benefits. The acquisition of firm assets is often designed to generate income or reduce expenditures, such as the purchase of equipment to boost revenue and profitability.

#2 - Equity Category

Equity account names include share capital, retained profits, and dividend accounts. They are not modified on a regular basis but rather in response to specific events, such as equity offerings or share repurchases. Changes to these titles require approval from the firm's senior authorities.

#3 - Revenue Category

The number of income sources determines the revenue division's number of account titles. A single title is adequate for a firm with a single source of revenue. Accrual accounting modifies these account names when a company gets a financial advantage or anticipates future economic benefits.

#4 - Expense Category

The term "expense category" refers to changes in account titles caused by financial transactions that have an impact on a company's economic benefits. This might happen when financial power shifts out or when a commitment that will be met as the economic gain increases. Transactions under this category can increase liabilities or decrease assets.

Examples

Let us look into a few examples to understand the concept better.

Example #1

Let us take the example of ABC Ltd; the company pays cash to purchase new machinery from another company. The accountant credits or adds the machinery account on ABC Ltd's general ledger for the cost of the new machinery. This adjusts the books to reflect that new machinery has been purchased and is now held by the company.

Similarly, the accountant will debit (deduct) the same amount from the cash account on the general ledger. This implies that the company paid for the new machinery in cash, and hence, the cost of the new acquisition has reduced the company's cash balance.

Example #2

The chart provided in the document outlines common account titles used in a company's financial statements. In businesses that generate both service and sales revenue, specific accounts are tailored to each type of income. For example, Accounts Payable is classified under current liabilities, with an average balance that is credited, while Accounts Receivable falls under current assets, and its average balance is debited.

Other account titles like Amortization Expense are categorized as operating expenses and typically recorded as a debit. These classifications are essential for organizing financial records and ensuring that accounts are correctly aligned with their respective categories in the financial statements.